The everyday investor may have never heard of collateralized loan obligations, otherwise known as CLO’s, but they are quickly becoming a major part of the structured financial market. CLO’s are debt instruments that have been around for over 30 years and have a proven track record of protecting principal while offering attractive returns for investors. CLO’s also give investors access to the loan market that has historically only been accessible to accredited investors. But are CLO’s right for everyone?

So, what are CLO’s? CLO’s are essentially a pool of senior secured loans, typically floating rate, to businesses that are rated below investment grade. Being senior secured, they rank ahead of all unsecured debt in the event of bankruptcy. At inception the CLO will raise money from investors by selling debt and equity tranches. Each tranche has a ranked claim on the cash flows received from the underlying loans. The AAA tranche has the highest claim with equity having the last claim being the most junior tranche. This waterfall structure creates subordination among the tranches with AAA tranche having the highest protection and the BB tranche with the lowest. The AAA tranche carries the lowest coupon but takes the least risk while the BB carries the highest coupon and the highest risk. Equity does not carry a coupon but represents a claim on all excess cashflows that remain after the obligations of the debt tranches have been met. When principal and interest are received on the loan pool the principal will be used to purchase new loans for the portfolio and the interest will be paid to the investors. This purchase of new loans and interest payments will continue until the end of the reinvestment period, which is usually 5 years. After the reinvestment period ends principal will be used to pay down the tranches starting with the AAA and moving down the capital structure.

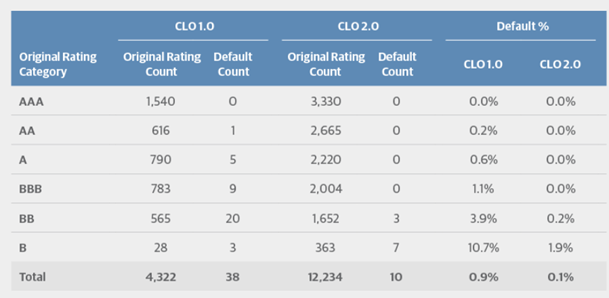

The structure of CLO’s is what gives them such great principal protection, even in an economic downturn. In fact, as you can see below there has never been a default in the AAA or AA rated CLO tranches of 2.0 CLO’s. CLO 2.0s were created in 2014 following new legislation enacted after the GFC that mandated tranches have higher subordination. Due to subordination the equity tranche and lower rated debt tranches will take on losses first. This gives investors extra principal protection.

Source: Guggenheim Investments, Standard and Poor’s. Data as of 6.30.2022.

In addition to the principal protections CLO’s offer, CLO’s can offer a higher return than traditional corporate bonds as you can see in the figure below. This is because despite the investment grade ratings of the top tranches, CLO’s still take exposure to below investment grade loans which have a higher yield. They are able to earn a higher credit rating due to diversification and credit enhancements built into the structure.

Source: JPMorgan, Bloomberg, BofAML. Data as of September 30, 2022. Past performance is no guarantee of future results. There is no guarantee that any investment strategy will achieve its objectives, generate profits or avoid losses.

So why doesn’t every investor include CLO’s in their fixed income allocations? Currently, there are only a few CLO ETF and mutual funds that are available to the average investor. To invest in individual CLO’s, investors must be considered a QIB or “Qualified Institutional Buyer” that owns or manages at least $100 million worth of securities. Because CLO’s are considered 144A securities and traded in the private markets instead of over a public exchange, they may also face liquidity issues in times of economic stress. This could cause large fluctuations in pricing which may not be suitable for some investors. In addition, even though AAA and AA CLO tranches have never defaulted in the past, this does not mean this could not happen in the future. CLO’s have many protections against defaults and loss of principal with the top-rated tranches being least risky, but this does not mean they are 100% full proof and investors should be aware of the potential risks.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Credit Analyst

Boyd Watterson Asset Management, LLC