As the debate around monetary policy remains lively, we remain focused on the trend of incoming macro and market data. While we cannot know with certainty what the Federal Reserve will do with the target rate, we can compare the current setup to the last time they decided to cut the target rate in 2019. The charts below, coupled with comments from the Fed, provide some context into how they were viewing the economy at that time and brings into question what has changed in how they view those same measures this time around.

“What we’ve been monitoring since the beginning of the year is, effectively, downside risks to that outlook from weakening global growth, and we see that everywhere: weak manufacturing, weak global growth now, particularly in the European Union and China.”

– Jerome Powell (July 31, 2019)

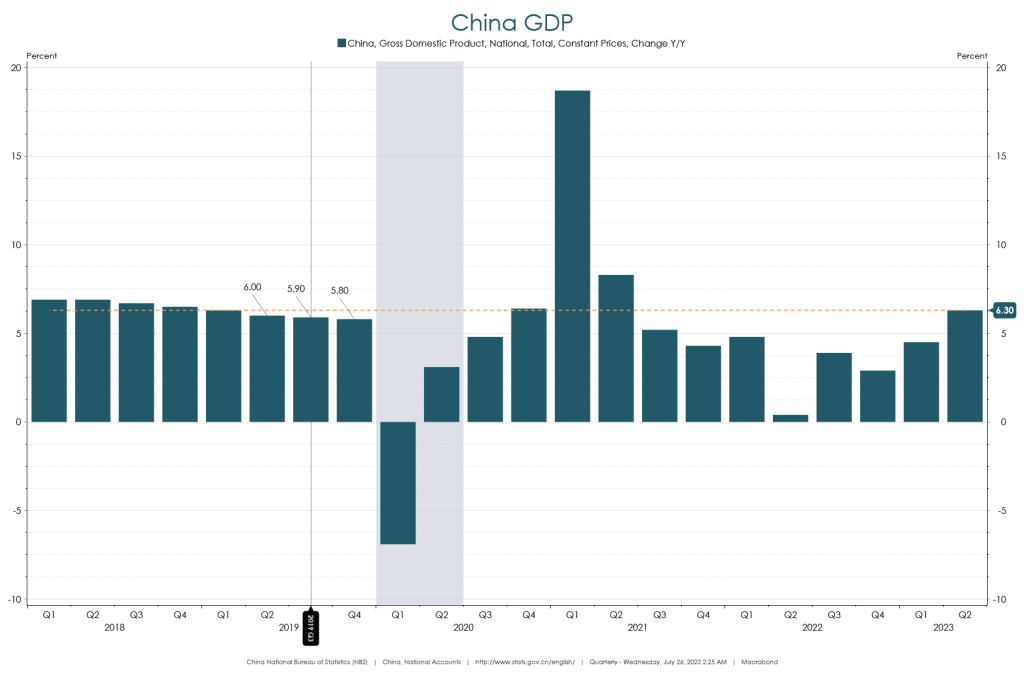

United States GDP accelerated to 2.6% y/y in 2Q23, 0.3% above where it was in 3Q19 and in line with the 4Q19 print. The q/q seasonally adjusted annualized rate accelerated to 2.4% in 2Q23, 0.3% lower than where it was in 2Q19 and 1.2% lower than the 3Q19 print. Euro Area GDP decelerated to 0.6% y/y in 2Q23, 1.2% lower than the 3Q19 print. China GDP accelerated to 6.3% y/y (easy comparison set due to Omicron lockdowns), just 0.4% better than where it was in 3Q19. Without raising concerns about the primary contributions to U.S. GDP and disregarding the easy Omicron comp for China, global growth is roughly in line with 2019 levels or worse (i.e. Europe).

Source: Macrobond.

“What you hear is that demand is weak for their products. You see manufacturing being weak all over the world. Investment—business investment is weak. And I wouldn’t lay all of that at the door of trade talks. I think there’s a—there’s a global business cycle happening with manufacturing and investment, and that’s—that’s been, you know, definitely a bigger factor than, certainly, we expected late last year. I think global—global growth started to slow down in the middle of last year, but that has gone on to a greater extent.”

– Jerome Powell (July 31, 2019)

United States industrial production has been negative on a y/y basis for two months in a row as of July. Leading up to the July 2019 rate cut, industrial production had been negative for three months (the negative print in July would not have been available yet). Manufacturing production from the U.S. has been negative y/y for five consecutive months, although not as negative as it was in 2019. Overseas, we observe a similar setup with Germany in negative territory and China below where it was in 2019.

Source: Macrobond.

“I think we look at a broad range of factors, and trade uncertainty—trade policy uncertainty is one of them. That certainly includes the discussions with China, but I wouldn’t—I wouldn’t be able to tell you how much of it is due to that. And without knowing—you know, I think we—with trade, we have to react to the developments, and we don’t know what they’ll be, and so it’s hard to exactly say. Certainly, we’ve seen, though, that when there’s a sharp confrontation between two large economies, you can see effects on business confidence pretty quickly and on financial markets pretty quickly”

– Jerome Powell (July 31, 2019)

Trade data from the U.S., Germany, and China has decelerated more on a y/y basis this year than they had in 2019. On the business confidence side, the effects can be seen in ISM PMIs from the U.S.

Source: Macrobond.

“Now, the engine, though, is really a consumer economy, which is 70 percent of the economy. The manufacturing economy—the investment and manufacturing part of the economy—is more or less not—not growing much. It’s at a healthy level but not growing much. So—and we hope to help that with this rate cut. But, I would say, overall, we’re trying to sustain the expansion and keep, you know, close to our statutory goals, which are maximum employment and stable prices.”

– Jerome Powell (July 31, 2019)

In 2019, Powell acknowledged the weakness coming out of the manufacturing economy but was comfortable with the labor market and inflation levels. Today, the unemployment rate remains historically low at 3.5%, slightly lower than where it was in July 2019. However, the labor force participation rate has remained unchanged at 62.6 for five months in a row and is below where it was in 2019.

Source: Macrobond.

On the inflation front, year-over-year growth rates remain above the FOMC target levels. However, price indexes have been trending lower and are close to the levels reached in 2019. The Goods PCE year-over-year growth rate dropped into negative territory in July and is in-line with where it was when the FOMC was cutting rates. The headline CPI year-over-year growth rate in July was 3.30%, above the FOMC target of 2% and higher than 2019. The current CPI growth rate is being impacted by the current near 8% year-over-year growth rate in shelter, which is a lagged measure of rental rates for owned and leased residential properties (real-time rental growth rates are lower than those being reported in the CPI). Excluding shelter, the year-over-year growth rate for CPI in July was 1.15%. The monthly growth rate in shelter has been slowing, as it catches up to current rental rates, which has caused the monthly growth rate of the CPI to slow to near 0.20% in recent months. If the CPI stays at that monthly growth rate, the year-over-year rate will decline to 2.2% in the first half of 2024.

Source: Macrobond.

There is some concern amongst the FOMC members that price measures could reaccelerate if monetary policy were to ease too early. The main driver of sustained increases in price measures comes from increased demand via rising real incomes and credit growth. We wrote a blog post last week highlighting the tightening credit conditions in the banking industry, making it unlikely that credit growth accelerates in the near term.

Real consumer incomes have been declining, as average hourly earnings have been increasing at a slower rate than price measures. The cumulative impact of negative real earnings growth will likely impact consumer spending moving forward. Moreover, the amount of spending that has been placed on credit cards has been growing near record paces over the last several months. This was also during a time when student loan payments were on pause – that ends October 1, 2023. While nominal retail sales accelerated in June to 3.1% y/y (-0.1% y/y on a real basis), the catalyst for further acceleration remains muted given the income and debt setup. Without an expansion in credit and positive real incomes, demand will likely decline, which makes it less likely that price measures can accelerate on a sustained basis.

Source: Macrobond.

“We think our policy stance is appropriate at the moment; we don’t see a strong case for moving it in either direction,” said Powell in May 2019, two months prior to the rate cut. Today, he has talked about the need to do more, but the market is not currently pricing that in. The market’s current expectations for Fed policy via the Fed Funds futures market have zero rate hikes priced in with possible rate cuts occurring around May 2024.

Source: Macrobond.

The major takeaway from this analysis is that the significant difference from today compared to 2019 is inflation, which appears to be slowing on its own as demand declines. As we move closer to the September 20th FOMC meeting, we will provide updates on the underlying economic trends that ultimately drive the path of interest rates and may influence the decisions of the Federal Reserve.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Investment Strategist

Boyd Watterson Asset Management, LLC