Over the last few quarters, we have been highlighting the trend in commercial banks’ ability and willingness to lend and what impact that might have on the economy. Last week, we received data from the Senior Loan Officer Opinion Survey (SLOOS) for 2Q23. Across most measures, banks remain at historically elevated levels, even in categories where there was slightly less tightening. The major takeaway from this update is that the trend in credit conditions remains weak and will likely have a negative impact on real economic activity moving forward.

Domestic banks reporting tighter standards on business loans increased to 47.3, the highest level since 3Q20, and the path has moved in a similar direction as 2000 and 2008. Underneath that, standards for Commercial Real Estate and Commercial & Industrial lending remain historically tight.

Source: Macrobond.

For banks that reported tighter standards, the reason for doing so being related to liquidity concerns and/or reduced risk taking increased to the highest level since 2Q20. If banks are concerned about their own balance sheet, they are less likely to lend and take on additional risk.

Source: Macrobond.

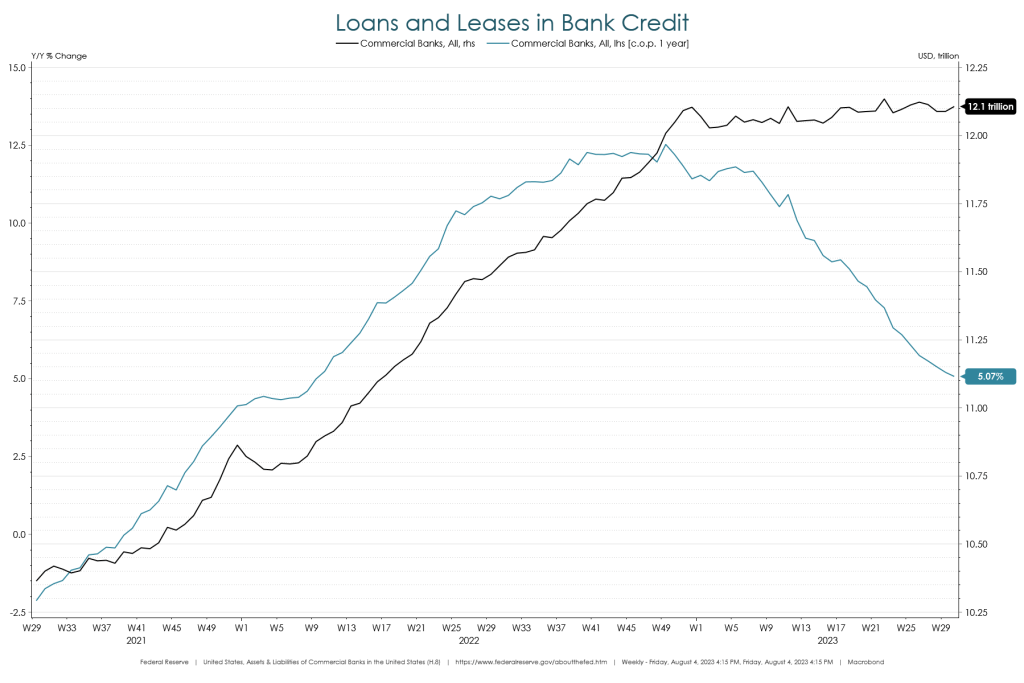

Turning to the current commercial bank setup, H.8 data from the Federal Reserve tracks commercial bank assets and lending on a weekly basis. The trend in 2023 is moving in a direction that corroborates the SLOOS data – a decline in assets and a slowdown in lending. Again, if bank balance sheets are impaired or expected to become impaired, they will likely reduce lending which has negative implications for real economic activity.

Source: Macrobond.

Outside of the United States, we are seeing a similar trend in lending in the Euro Area. In the latest update from the ECB, Loans to Residents decelerated to 1.4% y/y and the value has essentially flatlined in 2023. Loans to Non-Financial Corporations decelerated to 2.2% y/y and has moved lower from the start of the year.

Source: Macrobond.

As we move through the second half of 2023, concerns surrounding the credit environment will likely garner more attention. We will continue to monitor this developing situation as more data becomes available.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Investment Strategist

Boyd Watterson Asset Management, LLC