In the last few weeks, we have been noting the weakness in economic data from the U.S. and corporate earnings. In our view, this indicates a slowdown occurring domestically, as well as a reflection of what we have seen in other countries. Given this is a global system, it is important to monitor and highlight macro data in different areas of the economy and across countries if they begin to move in a similar direction. To that point, we have seen decelerations in growth and inflation measures across most major economies over the last month.

Last week we received more European data that continued to move in a negative direction, which likely reflects a weaker global economic backdrop and may have negative implications for the U.S. economy. Using the broadest measure of growth, Euro Area GDP was revised lower to a year-on-year annualized rate of 1.0% in 1Q23, down compared to 1.8% in the prior quarter. Excluding the pandemic slowdown, this was the worst reading since 4Q13 when the region was recovering from the European sovereign debt crisis.

Source: Macrobond.

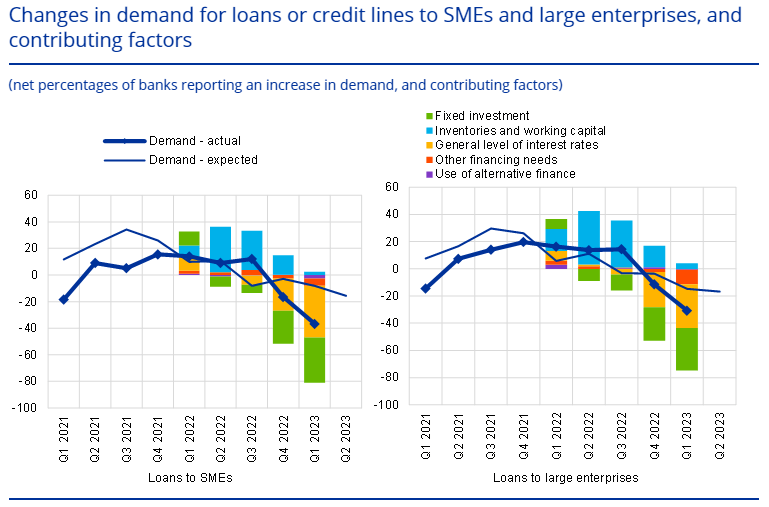

In addition to the deceleration in GDP, lending conditions continued to tighten in 1Q23 from an already elevated level moving out of 4Q22, according to the ECB Bank Lending Survey (BLS). Further tightening of lending standards likely leads to less credit growth, which tends to have negative implications for real economic growth.

“In the April 2023 BLS, Euro Area banks indicated that their credit standards for loans or credit lines to enterprises tightened further substantially in the first quarter of 2023. From a historical perspective, the pace of net tightening in credit standards remained at the highest level since the Euro Area sovereign debt crisis in 2011.”

Source: ECB.

Within the BLS, it is also worth noting the demand side of lending activity worsened, which typically occurs in periods of economic weakness.

“Firms’ net demand for loans fell strongly in the first quarter of 2023. The decline in net demand was stronger than expected by banks in the previous quarter and the strongest since the global financial crisis.”

Source: ECB.

In line with what we saw from the BLS, we have seen loans to households and non-financial corporations decelerate over the last few months.

Source: Macrobond.

For 1Q23, European growth slowed, credit conditions worsened, and the monthly data we have received since then has not improved. To review, Euro Area retail sales declined 2.6% y/y in April, marking the tenth month of negative y/y growth out of the last eleven. Italy retail sales decelerated to 3.2% y/y in April, down 300 basis points from the start of the year. More importantly for Italy, the seasonally-adjusted volume index for retail sales has been negative for several months.

Source: Macrobond.

The weakness in consumer spending, coupled with a negative outlook on credit growth, is also showing up in growth-related data. For example, German industrial production decelerated to 1.8% y/y, factory orders remain weak at -10.0%, and foreign trade slowed further with imports at -10.3% y/y and exports at 1.5% y/y. Spain and Italy also saw industrial production decelerate in April to -1.7% y/y and -7.2% y/y, respectively. This is likely a reflection of a weaker consumer setup and a decline in expectations for real economic growth. If the global economy was going to improve from where it was at the start of the year, these indicators would be moving in the other direction.

Source: Macrobond.

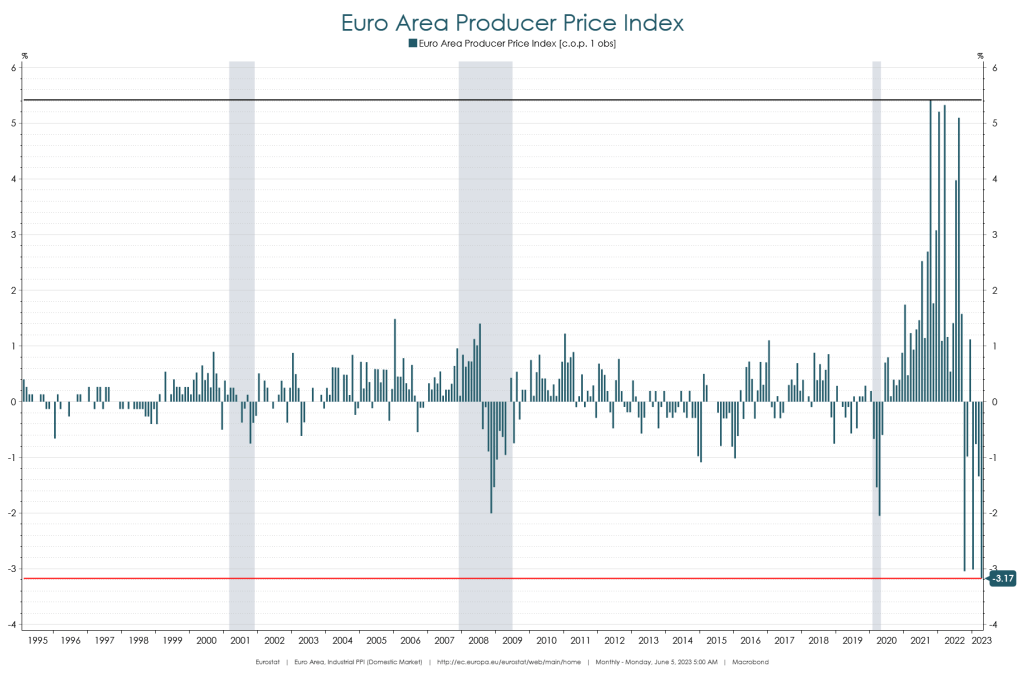

As growth measures have weakened, we have also seen inflation decelerate. The Euro Area Producer Price Index fell 3.2% m/m, its largest decline on record. On a rate of change basis, PPI has slowed at a record pace to 1.0% y/y in May from its peak of 43.4% in August 2022. For consumers, the Consumer Price Index in Germany decelerated to 6.1% y/y in May from 7.2% and Spain decelerated to 3.2% y/y in May from 4.1%. Prices falling at this rate is likely another indication of demand slowing, which we have observed in other macro indicators in Europe and globally.

Source: Macrobond.

The major takeaway from this data is that the European economic data has continued to decelerate and that weakness likely reflects a weaker global economic environment. This dynamic will likely have negative implications for the U.S. economy.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Investment Strategist

Boyd Watterson Asset Management, LLC