With COVID variants such as Delta and Omicron seemingly slowing down and back to office plans being put in effect, companies have begun to shift their focus on office space needs into 2022 and beyond. The U.S. office market registered its first quarter of positive net absorption in Q4 2021 since the onset of the pandemic, while continuing to deliver new office product to the market.

Data compiled by JLL shows that leasing activity increased 9.2% in Q4 2021, gaining back 71% of the quarterly levels seen before the pandemic with annual activity 14.6% above 2020 metrics. While many think that the pandemic brought on major headwinds for the sector’s larger leasing activity, there is still a need for larger and longer-term transactions. Leases over 100,000 square feet accounted for 43.6% of the annual activity. There was also a renewed interest in long-term commitments, as the average term length rose for the 4th consecutive quarter to 7.8 years of lease term.

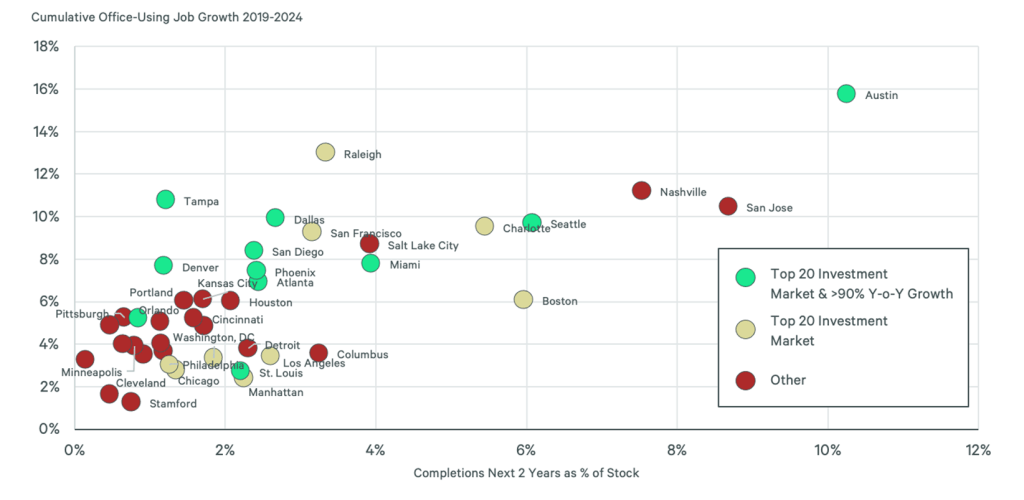

There has been a continuous debate throughout the pandemic on the impact of telework on leasing demand. Intuitively, one would think that technology firms would be leading the telework movement. On the contrary, technology firms have outpaced other sectors and remain the strongest driver of leasing activity, accounting for 21% of the Q4 2021 activity. The majority of this demand has been realized in the Sunbelt markets, such as Austin, Atlanta, Miami, etc. Technology demand as a result of the major relocations or “HQ2s” to these markets has had an immediate impact on job growth. Investor demand in these markets is a direct result of the job growth brought on by these tenants. Early in the pandemic, CBRE Research identified the markets with the most propensity for telework. Coincidentally, a trend began to form tying investor demand to the markets that were poised for the shift to telework, but in turn are projected to lead in office using job growth.

Source: CBRE Research

The strong investor demand in these markets is coming in the form of new development. According to Cushman and Wakefield’s Q4 Office report, new developments declined into the end of 2021 after peaking in mid-2020, but the market is still realizing construction levels 29% above the 10-year historical average. Tenant demand for these new deliveries amplifies the flight to quality trend that was a major theme of pre-pandemic leasing activity. Employers, now more than ever, are putting an emphasis on the tenant experience of their employees by focusing on workplaces that cater to health and wellness, work life balance, and amenity rich environments. This allows them to attract and retain high quality talent in what many consider to be a job seekers market.

The road to recovery for the U.S. Office market will not happen overnight. It projects to be carried out over a longer period and will look differently than the office environment of the past, but the evidence shows there is still a commitment to leasing office space.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Vice President, Asset Management

Boyd Watterson Asset Management, LLC