In 2018, municipals saw steady and strong demand across all maturities and sectors despite the heightened volatility in the taxable markets. Even as yields moved higher, the supply/demand imbalance in the municipal market provided enough support for investment grade municipals to post positive returns for the year.

In 2019, we have continued to see a similar story unfold in the municipal market, while the taxable markets have rebounded nicely, and have benefited from the Federal Reserve’s newfound “patient” approach to monetary policy. The demand for municipal bonds has continued to gain traction due to a variety of factors:

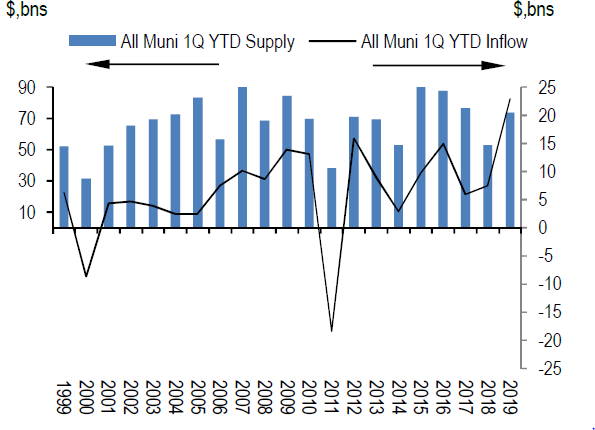

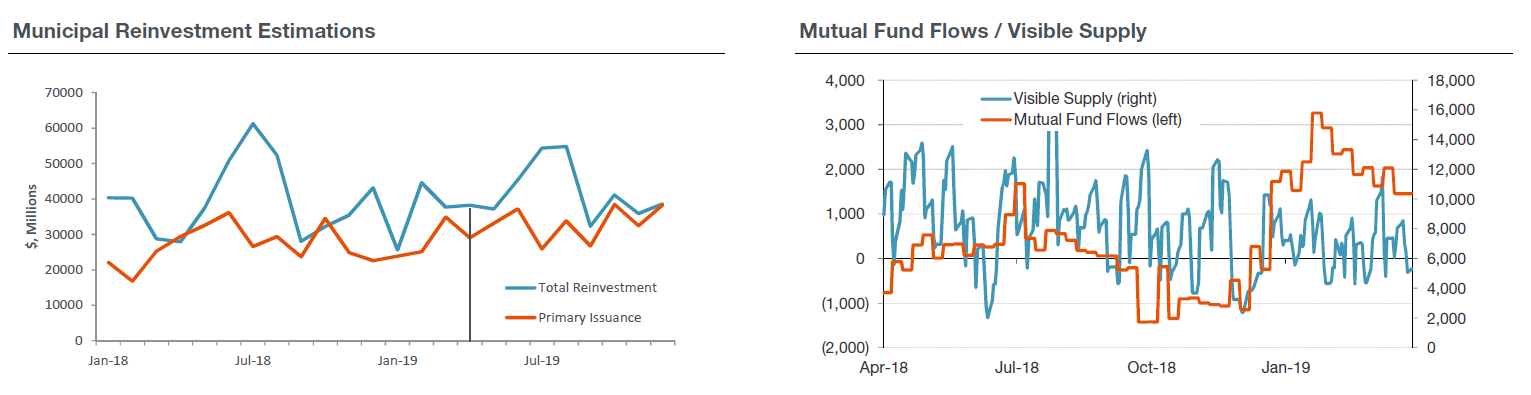

- The supply-demand imbalance persists. Issuance is 11% lower than the trailing 5-year average while inflows reached record first quarter highs.

Source: Lipper, Thomson Reuters, Bloomberg, JP Morgan. Fund flows as of March 27, 2019 and issuance as of March 31, 2019.

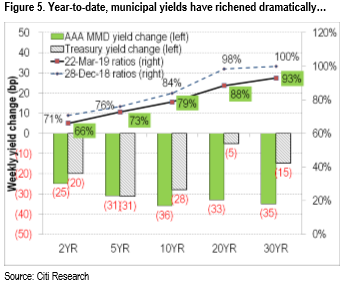

- The recent inflow of money into municipal mandates, particularly in separately managed accounts, has helped drive muni demand as investors have tried to minimize the impact of the tax code changes. As a result, ten-year municipal bonds are trading at their tightest levels relative to U.S. Treasuries in over 19 years.

- This persistent, strong demand is partially due to the new tax laws and the $10,000 federal limit on state on local tax deductions (SALT). As a result of the tax law changes, wealthy investors are finding themselves paying more in taxes, particularly in states such as California, Connecticut, Minnesota, New Jersey, New York, South Carolina and Wisconsin. As high net worth clients file their taxes and begin to realize the effects of the changes, we believe the demand for munis will continue, particularly in those states impacted the most.

Source: Piper Jaffray.

What we are closely monitoring:

While the wind appears to be at the back of municipal investors, the unfunded pension liabilities of State and Local Governments remains a top concern of ours and should not to be overlooked. Perhaps the biggest issue is the estimated $6 trillion in unfunded pension liabilities facing these entities. At the state level, the unfunded liability is estimated at $1.4 trillion for a funding level of only 66% of liabilities, which is down from being fully funded in 2001. Some reasons for the funding gap include the following:

- Investment returns that fall short of aggressive actuarial assumptions (average 7.6%)

- Longer average life expectancy, meaning pensions must pay out benefits over a longer period of time

- State and local governments not making the necessary contributions

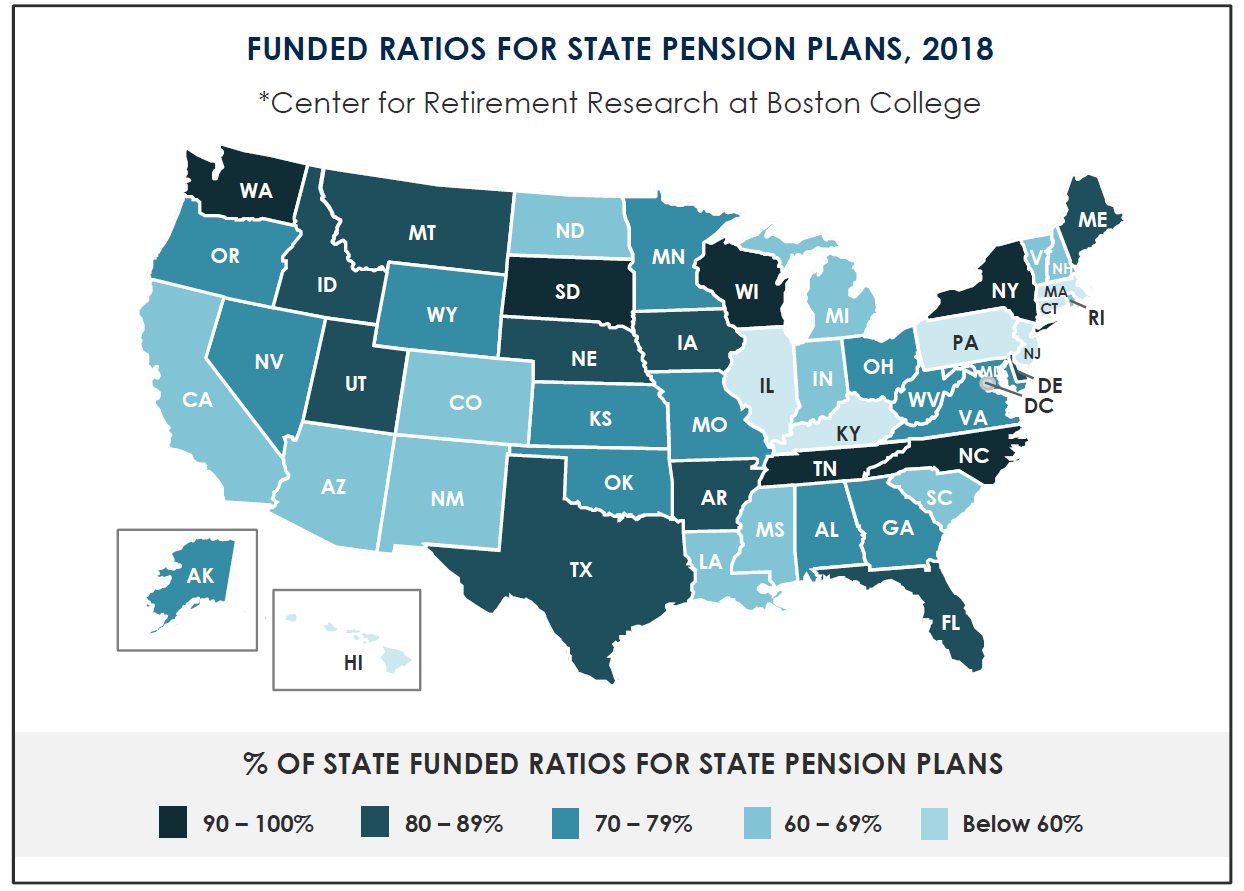

The funding levels differ greatly between states. For instance, states like Wisconsin, South Dakota, Tennessee, and New York are all well-funded with funding ratios of 90% or higher. On the other hand, states like Kentucky, New Jersey and Illinois, find themselves well underfunded with funding ratios in the 31% to 36% range.

Source: The Pew Charitable Trusts and American Legislative Exchange Council.

Although pension funding remains a concern, other post-employment benefit (OPEB) liabilities are also escalating rapidly which could affect local government spending and infrastructure priorities. Monitoring pension and OPEB liabilities is an essential aspect of the municipal bond investment process at Boyd Watterson. We leverage credit research performed by our Real Estate Investment Team for the Boyd Watterson State Government Strategy (a real estate strategy that focuses on investing predominately in properties leased to state and local government agencies). Our philosophy takes a strategic view of macroeconomic and market factors, while focusing on the preservation of capital. This leads us to emphasize high quality securities, eliminating a number of municipalities from investment consideration due to quality concerns which often include unfunded pension and OPEB liabilities.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC