As mentioned in prior posts, we currently have a more favorable view on the fundamentals of the consumer and commercial real estate market than the corporate market. To express that theme, we favorably view assets that have exposure to the consumer and to real estate. In general, the consumer is in good financial shape due to low interest rates, nearly full employment, improved balance sheets (debt reduction and asset value appreciation due to equity market gains). That has led us to increase our exposure to ABS and MBS securities.

Asset backed security returns have lagged those of short corporate securities YTD, but in our opinion have a much better credit quality profile. ABS are less liquid relative to short corporates, but we are willing to make that trade due to the attractive relative value of ABS.

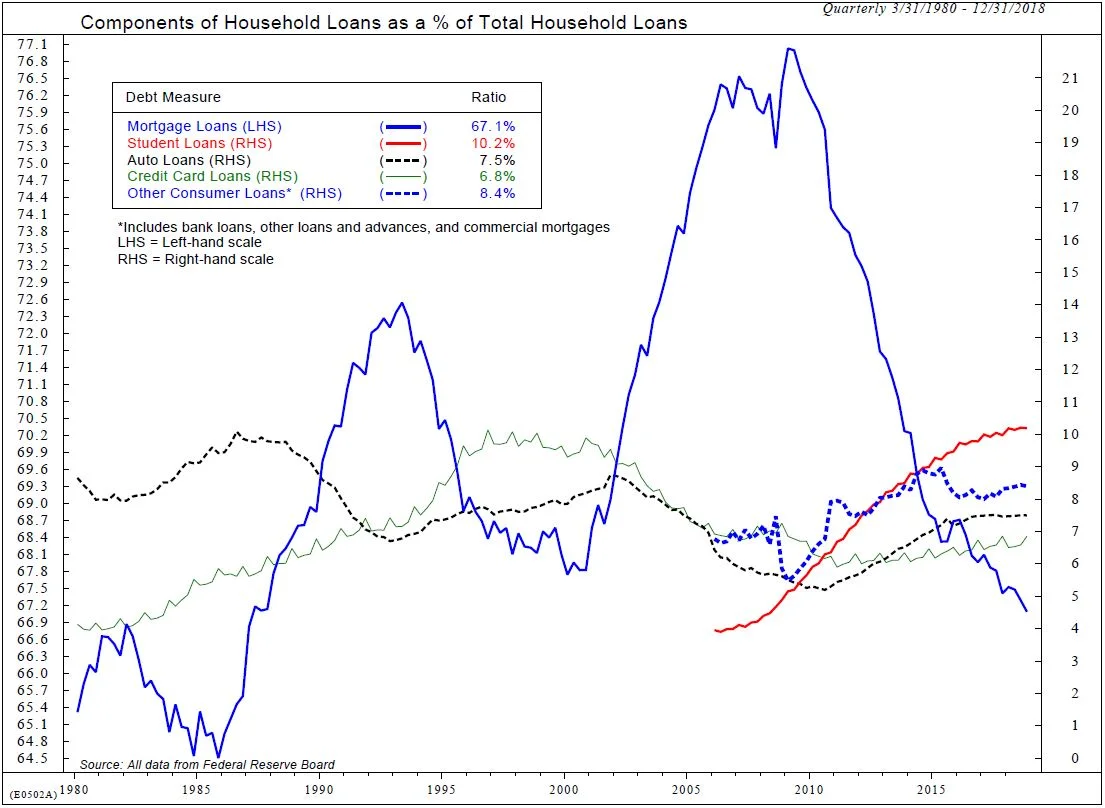

We have also added non-agency MBS to portfolios. Again, the theme of the consumer is a driver of this trade. Mortgage debt as a percent of total household debt has declined to levels last seen in the mid to late 1980s and delinquency rates are as low as they have been going back to 1980.

Copyright 2019 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at http://www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

From a valuation perspective, mortgages look fairly-priced in our view, but we believe offer much better protection should the economy show signs of weakness.

Lastly, we have added CMBS. We believe the commercial real estate market is in balance with limited new supply and plenty of investor demand for properties. From a valuation standpoint, CMBS looks attractive relative to corporate credit and offers higher yields for similarly rated securities. Much like the ABS market, CMBS have limited liquidity compared to corporates. Within CMBS, our strategy has been to purchase seasoned deals (deals issued in 2011-2015) as the market was just coming back to life post Great Recession and underwriting standards were extremely robust. We also favor seasoned CMBS because many of the properties in these deals have appreciated significantly and therefore, the loan to value ratios should be fairly low if marked to market. The building owners should not have a difficult time refinancing the loans even if property values declined from current levels.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC