Coming into the year, Chinese macro data was expected by many to rebound and provide a lift to global economic activity. The failure to meet those expectations and continued weakness across most growth and inflation measures will likely have negative implications for global economic activity, including the United States.

On a y/y basis, real GDP came in at 4.5% in 1Q23 and 6.3% in 2Q23. Despite the easy Omicron comp set, these are two of the slowest growth rates on record excluding the pandemic period. Additionally, as demand has slowed and inflation has decelerated, nominal GDP came in at 4.8% y/y, down from 5.0% in the prior quarter.

Source: Macrobond.

Turning the focus to consumer demand in China (internal consumption was supposed to be a primary driver of growth for 2023), retail sales for July decelerated to 2.5% y/y from 3.1%. Similar to other key macro indicators, this would be the weakest growth rate on record outside of the pandemic period. One way to get a view into China’s broader demand setup is through import data. For July, imports decelerated to -13.2% y/y, their slowest pace since May 2020.

Source: Macrobond.

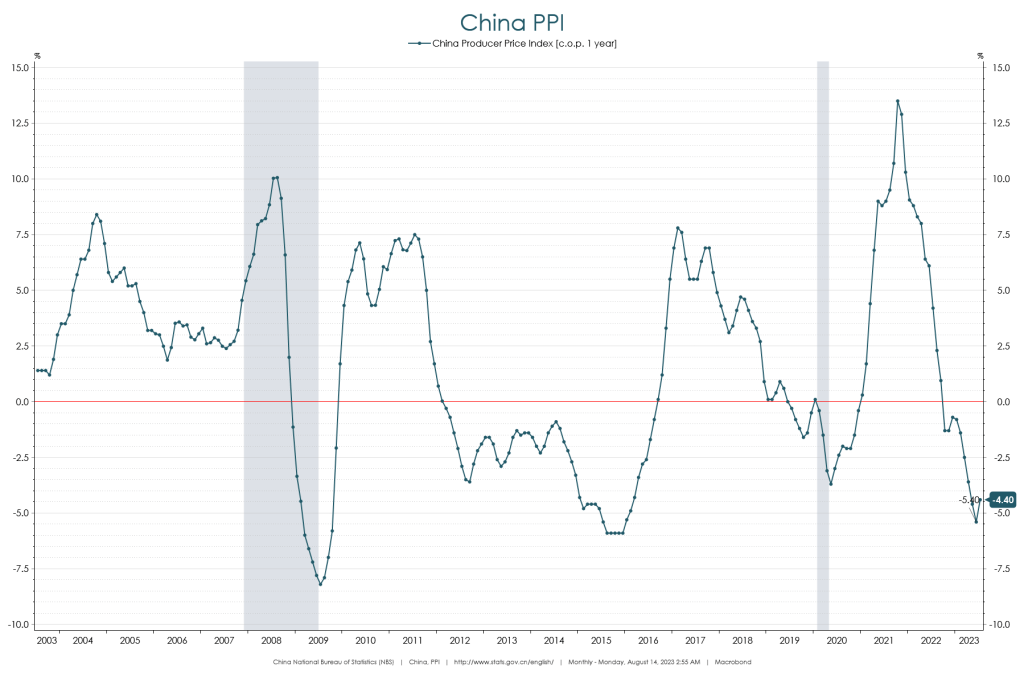

Another way to measure demand is through prices. Consumer prices for July decelerated to -0.3% y/y from 0%. Producer prices have been negative for ten consecutive months now, coming in at -4.4% y/y for July. Both of these measures are indications that demand has come down.

Source: Macrobond.

On the business sentiment side, NBS Manufacturing PMI data came in at 49.3 for July, its fourth consecutive month in contraction. Underneath that, new orders were in contraction for the fourth month in a row at 49.5 for July. New export orders fell deeper into contraction to 46.3 from 46.4 in the prior month. The Services PMI, an area of the economy that was supposed to drive a China rebound, has declined for four months in a row to 51.5.

Source: Macrobond.

With that sentiment setup in mind, we have seen weaker industrial production, industrial profits, and fixed asset investment. For July, industrial production slowed to 3.7% y/y from 4.4%. The y/y percent change in industrial profits remains negative at -16.8%. Private fixed asset investment decelerated further to -0.5% y/y, making another new record low excluding the pandemic.

Source: Macrobond.

Weaker global demand likely has a negative impact on the macro data previously mentioned. For a view into that global demand setup, Chinese export data decelerated to -15.4% y/y in July, down from -13.9%. The mix of who they export to has also tilted away from the U.S. and Europe in recent months, resulting in lower total volumes.

Source: Macrobond.

Market-based signals like USD/CNY, industrial metals, and Chinese equity prices have been moving in a direction that would suggest economic activity in China is expected to continue slowing. On the FX side, the U.S. Dollar improving versus the Yuan increases the cost of doing business internationally – this is near its highest level since 2008 at 7.21. Industrial metals such as Steel, Copper, and more remain weak on a y/y basis and are well below their pandemic highs. Two of the more notable equity indexes for China, the Shanghai Composite Index and Hang Seng China 50 Index, have continued to make lower highs since their cycle highs made in 2021. If the rebound was significant, or occurred at all, and macro data was going to improve from here, these market signals would likely be heading in the other direction.

Source: Macrobond.

A less than robust first half rebound and more economic weakness in China for July, coupled with worsening market data, likely points toward a slowdown in Chinese economic activity. As we move through 2023, we will continue to monitor China and the rest of global macro backdrop because it will likely impact the path of the U.S. economy.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Investment Strategist

Boyd Watterson Asset Management, LLC