In July of last year, we highlighted the historically fast pace of inventory accumulation over a period when producer prices were elevated. Additionally, over the last two years, we have observed a record-setting stretch of negative real average hourly earnings growth on a y/y basis. We have continued to highlight that the negative consumer setup would likely result in slowing demand. With that mix of expensive inventories accelerating and demand decelerating, we believed we would likely see corporate profitability slow over the coming quarters. Ultimately, a slowdown on the corporate side will likely have broad negative implications for other areas of the economy, including labor.

For 1Q23, corporate profits after tax without inventory valuation assumptions and capital consumption adjustments decelerated to -6.0% y/y, down compared to -1.4% last quarter. On a rate of change basis, this broad measure of corporate profits has slowed by 13% since 2Q22 and by more than 25% since 4Q21. This measure of corporate profitability is much broader than the S&P 500 or Nasdaq earnings alone. However, other measures of corporate profitability and both equity index earnings show a similar trend. As of the latest update from Bloomberg, S&P 500 earnings are down 3.6% y/y with 489 of 500 companies reported and NASDAQ earnings are down 9.8% y/y with 3,014 of 3,330 companies reported. This follows negative prints for both indexes last quarter.

Source: Macrobond.

It’s important to remember the economy and markets are not linear, but if demand and inflation slow further from here, it reduces the probability that profits will reaccelerate in the near-term to the 3.04 trillion high made in 2Q22. While we typically focus more on the rates of change, there has been a notable decline in the absolute level of profits over the last three quarters. In fact, the negative $170 billion change in value over the last year is the sixth largest decline on record and the y/y comparison set for 2Q23 is more difficult. A decline of this magnitude will likely change the way businesses operate going forward compared to the last two years.

Source: Macrobond.

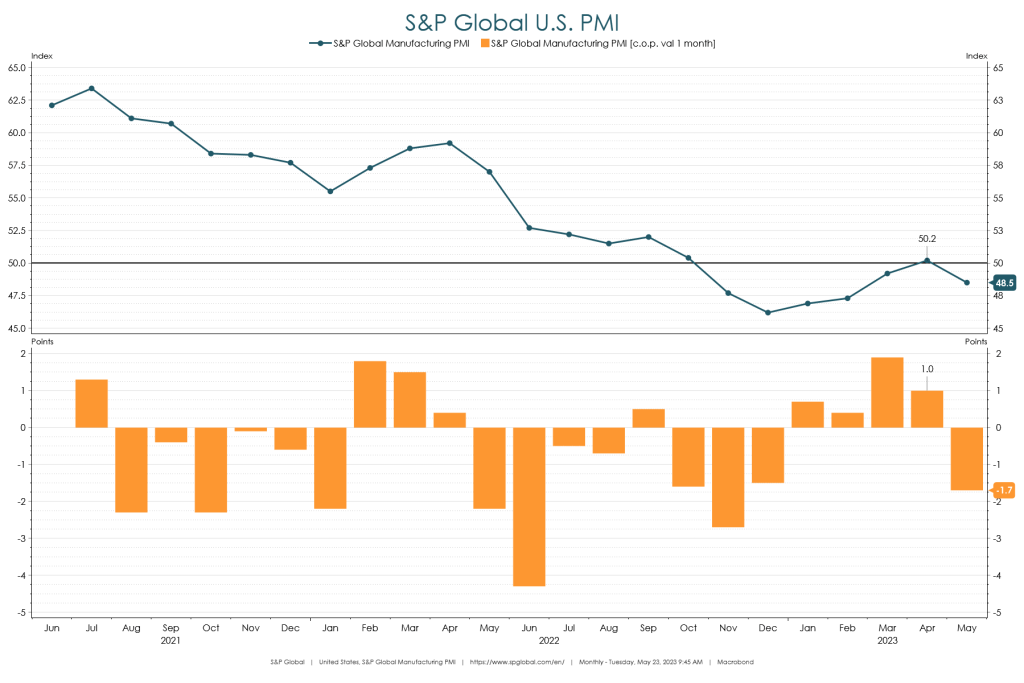

Since that data was captured, we have not seen meaningful improvement in the leading indicators we track. For example, nominal average hourly earnings averaged 4.5% y/y in 1Q23 and came in at 4.5% for April. Retail sales have decelerated from 7.4% y/y at the start of the year to 1.6% in April. Core durable goods orders were at 4.3% y/y in January and decelerated to 2.6% in April. Industrial production has decelerated to 0.2% y/y from 1.5% in January. The business sentiment side via the S&P Global Manufacturing PMI for the U.S. declined to 48.5 in May and has been in contraction in six of the last seven months. On the small business side, NFIB Small Business Survey data declined again in April and remains below the lows made during the 2020 recession.

Source: Macrobond.

We believe a deceleration in corporate profitability will likely eventually make its way into labor market data. Payrolls and earnings data will be released later this week. However, this data tends to weaken on a lag relative to other indicators as we have noted in prior posts. One way to track more near-term jobs data is through initial jobless claims which have been trending higher since September, though from a historically low level. Additionally, the increase in WARN notices should provide some insight into the direction of initial claims over the next few quarters.

Source: Macrobond.

The major takeaway from this analysis is that profitability has already slowed, and leading macro indicators have not moved in the direction that would suggest we will see a reversal of that trend in 2Q23. Therefore, it is becoming increasingly likely that a continuation of negative corporate profits from here will be a headwind for other areas of the economy.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Investment Strategist

Boyd Watterson Asset Management, LLC