At the beginning of the year there was a lot of conversation around a resilient consumer as the Personal Consumption Expenditures component of GDP accelerated. After that release, we highlighted the intra-quarter downward trend in that measure using the monthly series. More recently, we have seen spending trend lower in the monthly U.S. Census Bureau Retail Sales report and the weekly Redbook Retail Sales report. Given the weak consumer income setup, we believed January spending was not a reversal of trend and would likely decelerate as it had been in 2022.

Retail sales decelerated to 1.6% y/y in April from 2.4% in the prior month. This was its slowest growth rate since May 2020. It’s important to remember this data is reported in nominal terms, so with the Consumer Price Index at 5.0%, the real y/y growth rate is negative. Therefore, the y/y acceleration in retail sales reflects an increase in prices, not an increase in units sold. This means consumers are paying more and getting less.

Source: Macrobond.

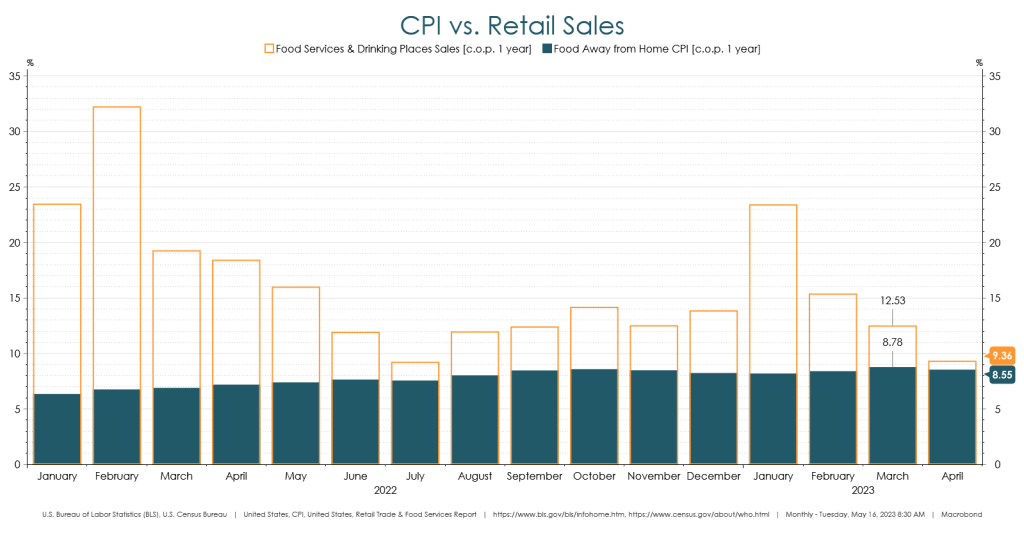

Critically, non-discretionary items related to food have led the headline sales number. Food services and drinking places sales accelerated 9.4% y/y while food away from home CPI accelerated 8.6%, and the spread between sales and prices in these categories has tightened since January, reflecting a slowdown in unit growth. Grocery store sales accelerated 3.7% y/y while food at home CPI accelerated 7.1%, reflecting negative unit growth. Again, most of the advance in food sales reflects price growth and not unit growth. If consumers are spending more and getting less on food, their ability to spend on discretionary items likely declines.

Source: Macrobond.

Another way to track consumer spending is through the weekly Redbook retail sales report, which accounts for roughly 80% of the Census Bureau report. As a weekly data set, there is more reporting than the monthly Census Bureau data, but the trend in the rate of change has been decelerating since the beginning of 2022. On a y/y basis, sales have been below 2.0% over the last six weeks, the weakest stretch since the negative prints made through the first half of August 2020. It’s also worth nothing that this series does include groceries, which as highlighted above have increased mostly due to price increases. Therefore, the broader mix is likely even weaker than the already weak y/y growth rates we have seen over the last few weeks.

Source: Macrobond.

The major takeaway from the sales data is the weakness in spending outside of essential items. Ultimately, it is the discretionary piece of spending that would indicate a strong consumer, not spending more on food.

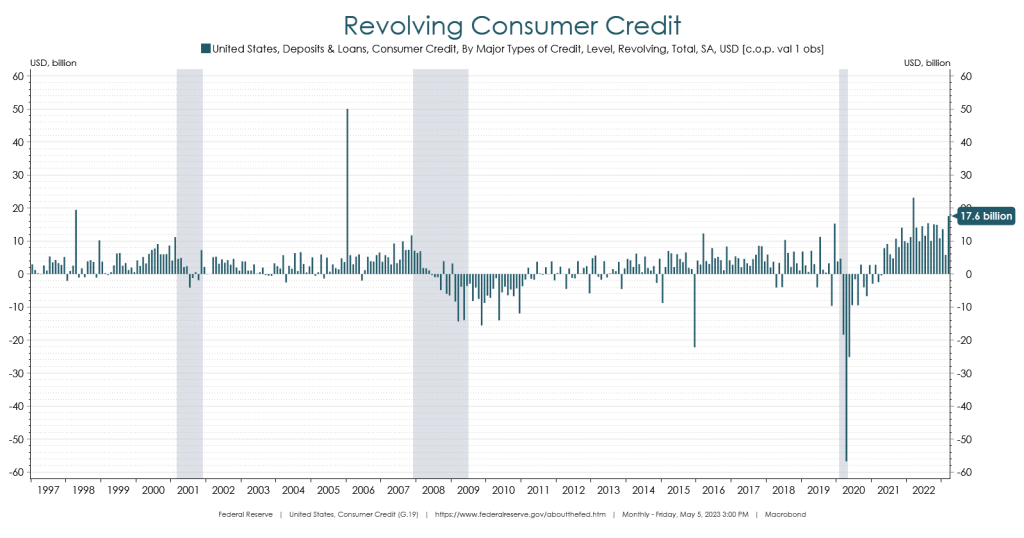

Another development is how much of that spending is occurring on credit cards. The latest update in revolving credit usage showed the fourth largest m/m increase on record. Additionally, the interest rates charged on those loans are at an all-time high. Given the decline in real average hourly earnings over the last two years and further tightening of standards from the 1Q23 Senior Loan Officer Opinion Survey data, we believe the setup for spending remains weak.

Source: Macrobond.

Away from the macro data, we have seen more evidence of a slowdown in consumer’s ability to spend from company reports. On May 2nd, Costco reported sales results for the month of April. Food sales led all categories, hitting high single digits y/y, similar to where food CPI was at for the period which means unit growth was most likely closer to flat. Nonfoods were negative low single digits, which highlights the divergence in non-discretionary and discretionary spending we observed in the macro data. On May 16th, Home Depot reported, “…further softening of demand relative to our expectations and continued uncertainty regarding consumer demand patterns, we are updating our guidance to reflect a range of potential outcomes. We now expect fiscal 2023 sales and comp sales to decline between 2% and 5%.” On May 17th, Target reported earnings and noted, “…pressure from inflation and rising interest rates affected the mix of retail spending in Q1, with a further softening in discretionary categories in the March and April time frame. This coincided with the deterioration in consumer confidence, reflecting recent events such as the banking crisis that emerged in March.”

Indeed, consumer sentiment as gathered by the University of Michigan survey has declined. The current conditions and expectations indexes declined m/m to 64.5 and 53.4, respectively. Both indexes are below where they were to start the year. The personal finances component declined to 87.0 and is also below where it was in January.

Source: Macrobond.

So far in 2Q23, we have not seen evidence to suggest the consumer is as resilient as projected coming out of 1Q23, which has negative implications for the rest of the economy. Over the next few weeks, we will be monitoring consumer-oriented company earnings and provide updates on this developing situation.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Investment Strategist

Boyd Watterson Asset Management, LLC