Since the bank failures in March, the conversation around a possible recession has shifted more firmly toward ‘when’ not ‘if’. However, there are Fed officials and financial commentators noting the recent labor market data as an indicator for strength in the economy.

“Despite the slowdown in growth, the labor market remains extremely tight. The unemployment rate was 3.4 percent in January, its lowest level since 1969. Job gains remained very strong in January, while the supply of labor has continued to lag. As of the end of December, there were 1.9 job openings for each unemployed individual, close to the all-time peak recorded last March, while unemployment insurance claims have remained near historical lows.” – Jerome Powell (March 8, 2023)

“You don’t have a recession when you have 500,000 jobs and the lowest unemployment rate in 50 years.” – Janet Yellen (February 6, 2023)

In environments like this, where economic data appears to be mixed, it is important to distinguish between leading and lagging indicators. Historically, labor market data tends to lag other measures of economic activity. Today, we are seeing more evidence of a slowdown in economic growth and inflation, which in our view likely portends labor market weakness. The lists below highlight some of the bigger picture macro trends we have been observing.

Growth:

- Manufacturing Orders – total manufacturing orders have slowed to 2.7% y/y, its slowest pace since February 2021, down to 536 billion from a peak of 554 billion in June 2022

- Manufacturing Backlogs – unfilled orders excluding transportation have decelerated to their slowest pace since April 2017

- Business Inventories – wholesale inventory growth accelerated at a record pace while the cost of accumulating that inventory was elevated

- Business Sentiment – ISM Manufacturing PMI remains in contractionary territory and has been for five consecutive months

- Consumer Income – real average hourly earnings have been negative for twenty-three consecutive months on a y/y basis

- Consumer Spending – real retail sales have not accelerated by more than 1.5% over the last eleven months and have been negative y/y in six of those months

- Consumer Savings – personal saving rate has been below 5% since January 2022

- Consumer Sentiment – the University of Michigan Consumer Sentiment Index has been near levels last seen in 1974, 1980, 1982, 1990, and 2008

- Consumer Debt – credit card use has accelerated at a record pace over the last quarter while the average interest rate charged on those loans is at all-time highs

Inflation:

- Consumer Prices – CPI has decelerated for nine consecutive months from 8.9% y/y in June 2022 to 5.0% in March

- Home Prices – the S&P Case-Shiller Home Price Index has decelerated to 3.8% y/y from 20.8% in March 2022, which is the fastest rate of change on record

- Auto Prices – The Manheim Used Vehicle Value Index has been negative y/y since September 2022

- Producer Prices – PPI has decelerated to 4.6% y/y from 11.6% in March 2022

It is the synchronicity of the weakness in these measures that helps us determine where we are most likely at in the cycle. Shifting the focus back to the labor market, the direction of jobless claims, payrolls, and the unemployment rate is likely to follow the data noted above. Looking at prior economic slowdowns, there is evidence that labor measures tend to hit their best levels just as the recession begins. Therefore, using them as a guide for where the cycle is at or going could be misleading. Another important takeaway is the amount of time it takes for the labor market to fully recover following a recession, whether it be a deep or shallow recession.

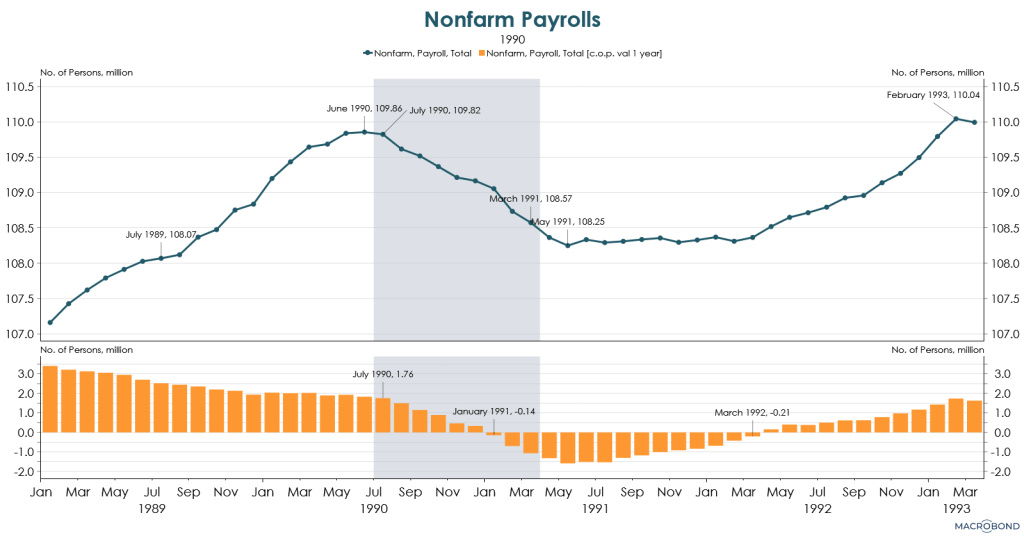

The charts below are examples of labor market data in 1990, 2001, and 2008.

Initial claims were at relatively low levels leading up to the recessions, peaking toward the end of the period. Continuing claims, which can be used as a proxy for how difficult it is to obtain a job after the initial claim is filed, did not recover to pre-recession levels for several years.

Source: Macrobond.

Nonfarm payrolls peaked close to the start of the recession and failed to recover for several years following.

Source: Macrobond.

One of the most commonly used indicators for the health of the labor market is the unemployment rate. In prior slowdowns, this tended to look strongest just before the recession began. Similar to claims and payroll data, the unemployment rate took several years to recover following a recession.

Source: Macrobond.

Moving away from the more traditional macro data, layoff announcements have been picking up since the fourth quarter of last year. One way to track these is to monitor WARN notices. Given the recent acceleration in notices (and broad economic weakness noted above), it is likely that these will make their way into initial jobless claims over the next year.

Source: Macrobond.

Turning to where we are today, initial claims have picked up slightly in 2023 but remain historically low at 228,000. Similarly, continuing claims have been trending higher to 1.823 million but are still relatively low. Nonfarm Payrolls for the month of March came in lower m/m at 236,000 and have decelerated y/y, but remain relatively healthy. Lastly, the unemployment rate is near record lows at 3.5%.

Source: Macrobond.

The big takeaway from the historical context is to recognize it is not unusual to see strong labor market data even if the cycle is turning. At this point, the data we track points to the cycle continuing to slow and we would expect the labor market to follow on a lag.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Investment Strategist

Boyd Watterson Asset Management, LLC