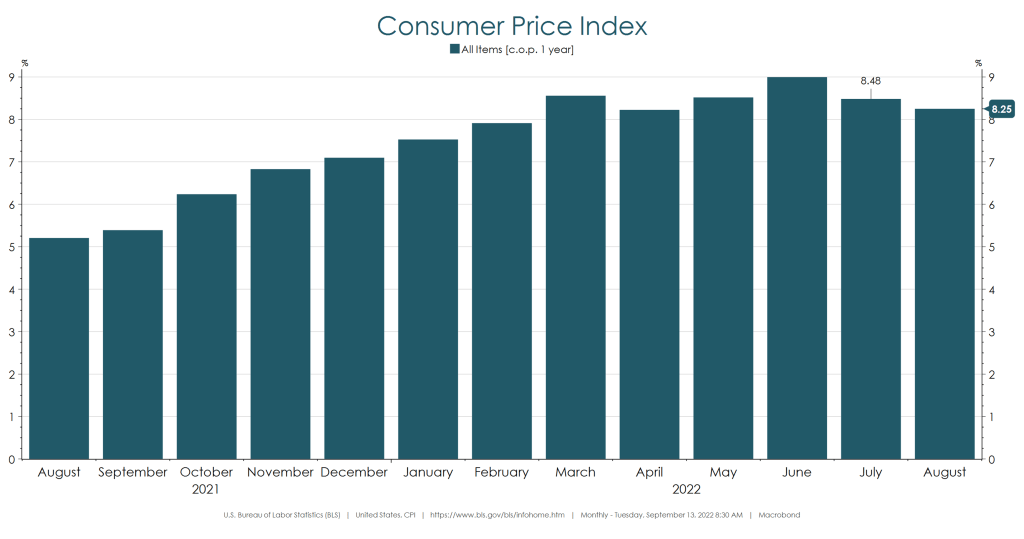

The headline Consumer Price Index number came in at 8.3% y/y for the month of August. While still at elevated absolute levels, it was a rate of change deceleration from 8.5% in July and 9.0% in June. On a m/m basis, CPI accelerated 0.12%, following -0.02% in July. Food prices accelerated 11.4% y/y, but the pace of the acceleration slowed versus the prior month. Energy prices accelerated 23.9% y/y compared to 32.9% last month and 41.5% in June, again the pace of acceleration slowed.

Source: Macrobond.

Core CPI, which excludes food and energy, accelerated to 6.3% y/y compared to 5.9% last month. Shelter makes up 33% of the headline reading and accelerated 6.3% y/y. Underneath Shelter, 24% of that component is Owners’ Equivalent Rent (OER) which accelerated 6.3% y/y. OER is based on the question, “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?” This measure of inflation is unique given that it is not actually a monthly cost to consumers. Additionally, Rent of Primary Residence makes up 7% of Shelter and accelerated 6.7% y/y. This component runs on a lag compared to asking-rents. So, while we are seeing rental rates slowdown, any deceleration in its contribution to CPI will likely not occur for several months. OER and Rent of Primary Residence will likely keep the headline and core CPI elevated in absolute terms.

Source: Macrobond.

Source: Hedgeye.

The market pricing in current, elevated absolute levels of inflation versus a rate of change slowdown in inflation is being reflected across the U.S. Treasury yield curve. The front end of the curve is pricing in rate hikes as the Fed continues to supply plenty of hawkish policy and commentary. In the last 90 days, the 3-Month is up 220 basis points, 6-Month is up 232 basis points, 1-Year is up 196 basis points, and the 2-Year is up 124 basis points. The long end of the curve has moved up by much less. On a 90-day basis, the 10-Year has moved up 56 basis points and the 30-Year is up 39 basis points. This suggests long-term, runaway inflation is less of a concern. This rate dynamic has resulted in an inverted yield curve, which historically is not a good sign for the economy.

Source: Macrobond.

Source: Bloomberg.

Other market-based indicators are also signaling a slowdown in inflation. The 5-year breakeven inflation rate and 10-year breakeven inflation rate are well below their highs reached in March and April. Additionally, 5-year and 10-year inflation swaps are well below their highs.

Source: Bloomberg.

Lastly, most commodities have decelerated on a 30-day and 90-day basis, and none of them are making new highs. In the last 90 days, WTI crude oil is down 25%, wheat is down 30%, oats are down 37%, lumber is down 35%, while steel, tin, aluminum, and iron ore are all down more than 20%.

Source: Bloomberg.

The market-based signals and slowdown in commodity prices are pointing towards a slowdown in inflation. So, while the market prices in rate hikes at the front end of the curve, the long end has not moved in a direction that suggests accelerating inflation is a long-term concern.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

*Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material or guarantee the accuracy or completeness of any information herein, nor does Bloomberg make any warranty, express or implied, as to the results to be obtained therefrom, and, to the maximum extent allowed by law, Bloomberg shall not have any liability or responsibility for injury or damages arising in connection therewith.

Investment Strategist

Boyd Watterson Asset Management, LLC