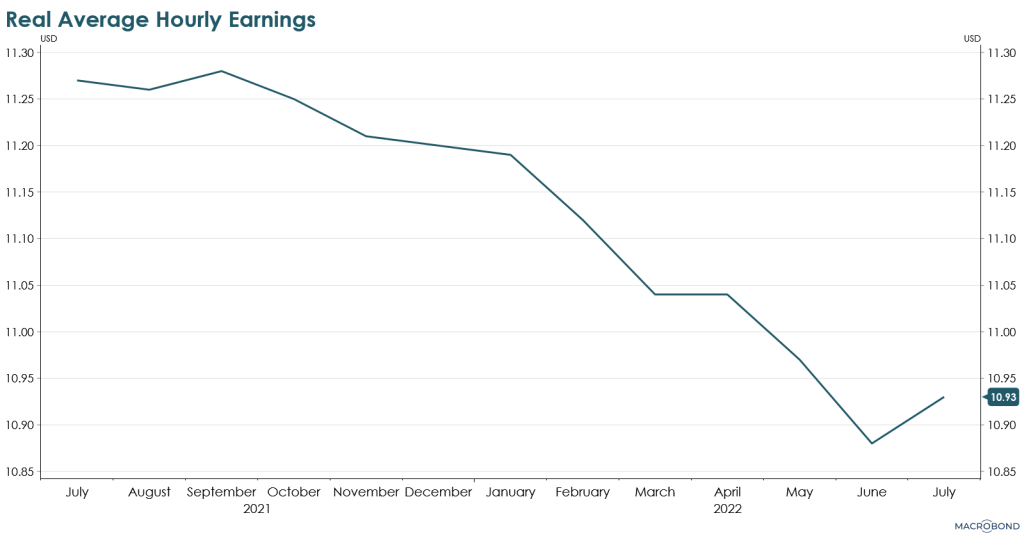

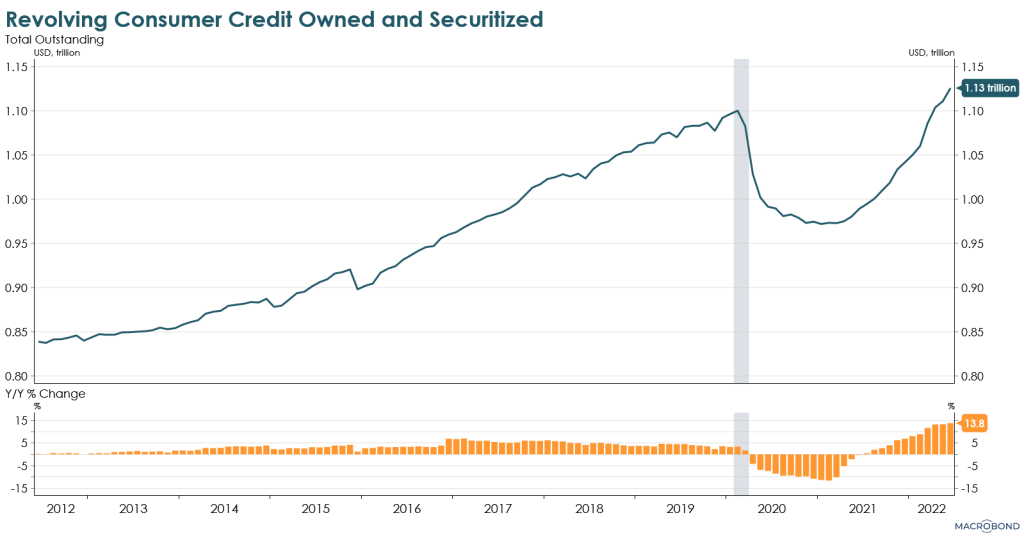

We have written about the slowdown in consumer related economic data multiple times, (May 25, 2022; June 15, 2022; April 6, 2022) driven by a deceleration in real earnings (combination of higher consumer prices and the expiration of fiscal support), leading to a decline in savings rates and an acceleration in consumer credit to try and maintain purchasing power (credit card and auto loan balances are at new highs and the pace of growth accelerated in 2021).

Source: US Bureau of Labor Statistics.

Source: US Bureau of Economic Analysis.

Source: Federal Reserve.

In two recent reports from the Federal Reserve, there was evidence that credit conditions are tightening and delinquency rates are starting to increase, especially for certain cohorts.

The Q2 2022 Federal Reserve Bank of New York Quarterly Report on Household Debt and Credit showed that 30-and 90-day delinquency rates have started to increase for credit card and auto loans.

Source: Federal Reserve Bank of New York.

Credit card and auto loan 90-day delinquencies are the most elevated for the 18-40 year old cohorts.

Source: Federal Reserve Bank of New York.

The same report also noted that credit card and auto loan delinquency rates are increasing for borrowers in the lowest income zip codes.

Source: Federal Reserve Bank of New York.

Consumer credit, especially auto and credit cards, has been rising as real earnings and savings rates have been declining.

Another report from the Federal Reserve showed that bank lending conditions for consumer loans have started to tighten. The percentage of banks that are tightening auto loans went from -14 in Q1 (meaning the majority of banks were loosening standards) to +2 in Q3 (meaning slightly more than half are tightening standards). For credit cards, the percentage of banks tightening standards went from -31 in Q1 to 0 in Q3. The percentage of banks reporting an increased willingness to make consumer loans has decreased from 24 in Q3 2021 to 5 in Q3.

Source: Federal Reserve.

These sizeable moves to tighten credit conditions normally occur during periods of economic slowdowns/recessions and can often mark the turning point in economic cycles. A lack of access to credit (demand for credit card loans are still rising) at a time of declining real incomes can cause a negative feedback loop and lead to declining consumer spending and a rise in delinquency rates. This phase of the cycle may be just starting to materialize.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC