Oil prices (West Texas Intermediate or WTI) have increased 40% from the low in early December 2021 to the highest level since 2014.

Source: Koyfin.

This may lead to an increase in the monthly growth rate of inflation measures like the consumer price index (CPI) and the producer price index (PPI). At the same time, other measures of inflation are not moving in the same way as oil prices, which is not uncommon. Oil prices have increased in prior periods that were not corroborated by other indicators and eventually economic growth, inflation, and oil prices moved in the direction of the other indicators.

During the current acceleration in oil prices, market-based measures of inflation like TIPS breakeven rates and inflation swaps made highs in November 2021 and have not followed oil prices in 2022.

Source: NDR.

The U.S. Treasury curve has also continued to flatten (short-term rates increasing more than long term) which typically happens when expectations for future economic growth and inflation are decreasing.

Source: Koyfin.

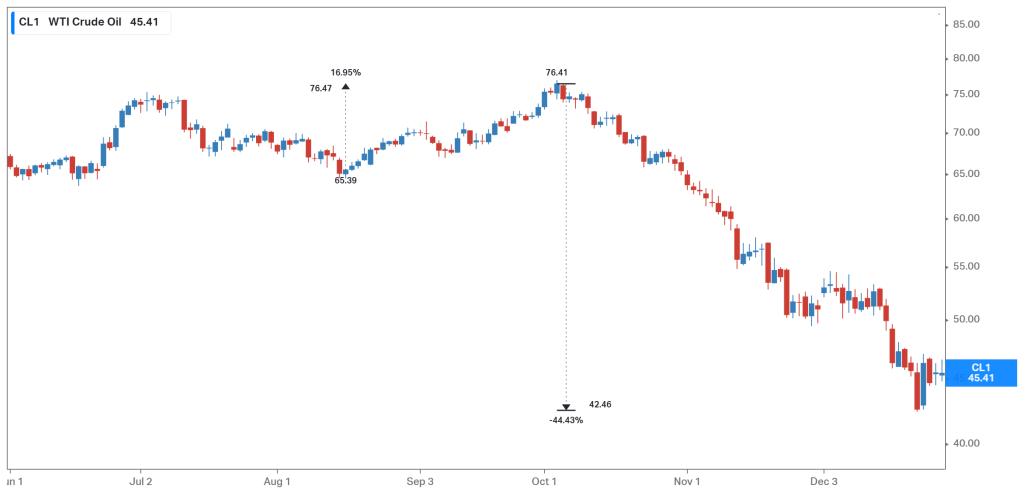

During the most recent period when the Federal Open Market Committee (FOMC) was increasing interest rates, oil prices rose over 15% during the summer of 2018, before peaking in October and declining 45% into the end of the year.

Source: Koyfin.

In 2018, TIPS breakeven rates peaked in May of 2018 and failed to make new highs with oil in October. Ten-year inflation swaps mostly moved sideways after May, getting briefly above that level in late September. Five-year swaps peaked in June and did not make a new high in October.

Source: NDR.

The Treasury yield curve was flattening throughout 2018 even while oil prices were increasing.

Source: Koyfin.

Going back further and looking at recessions for the last 30 years, oil prices tend to increase and then peak towards the beginning of the recession.

Source: FRED.

Part of the reason economic growth and inflation slow following large increases in oil prices is that consumer spending is negatively impacted by higher gasoline prices.

Source: FRED.

Market based measures of inflation are not moving in the same direction as oil prices. In prior periods when this has taken place, higher gasoline prices during a period of declining economic growth led to lower consumer spending, which pulls oil prices down in the direction of other measures of inflation. 2022 will likely end up being a similar dynamic.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC