This was another volatile week but provided some more signals regarding how investors are viewing growth and inflation trends in the U.S. and global markets, the impact of the new variant, and the diverging trends across different asset classes and geographies.

In the commodity space, energy-oriented areas like oil and natural gas declined again and volatility levels remain elevated. Oil prices are down 20% from their recent high and got close to their August low. Natural gas prices are down 35% from their recent high but remain above their August low.

Source: Koyfin.

Oil volatility is down from the recent high but remains elevated and well above the prior trend. The volatility level for natural gas prices has also spiked and remained elevated.

Source: Koyfin.

The London Metal Index is down 9% from the recent high but remains above the summer lows.

Source: Koyfin.

Agriculture based commodities like coffee, corn, and wheat are still showing positive trends as is the overall agriculture index.

Source: Koyfin.

Volatility levels for agriculture commodities (excluding corn) have been increasing, which could be a likely precursor to falling prices.

Source: Koyfin.

Commodities, especially energy, are leading indicators for future levels and direction of inflation. The current market signals are suggesting that inflation levels will likely decelerate in the coming months. If the recent trends continue, inflation levels may peak and start to move back to levels closer to 1-2%.

In fixed income markets, 10-year interest rates declined again in the U.S. and across global developed market economies. Yields remained above their August lows but are close to declining below the low end of the range they have been in since the end of September (Germany is already below).

Source: Koyfin.

The ten-year/two-year yield curve in the U.S. continued to flatten last week (down another 25bps) and ended the week at the lowest level in a year. Other developed market yield curves continued to flatten but not to the same degree as the U.S.

Source: Koyfin.

Within the U.S., the 30-year Treasury has dropped to record low level compared to the 20-year Treasury.

Source: Koyfin.

Expectations for future short term interest rates have also recently declined. The expectation for one month overnight index swap (OIS) in three years is now lower than the two year expectation. The expectations for short term rates on foreign holdings of US deposits (3-month Eurodollar rates) has also been declining and the curve has become slightly inverted.

Source: NDR.

Source: Bloomberg.

The movements in these curves suggest investors are starting to expect that short term interest rates will likely only increase for a short period of time before they start to decrease again.

Unlike the volatility levels in commodities and equities, the MOVE index (which measures US Treasury volatility) declined last week. Typically, declines in treasury volatility lead to declines in interest rates.

Source: Merrill Lynch.

All of the above mentioned movements suggest that investors are expecting inflation levels to start decelerating. Government bond yield curves have not fully inverted yet and short-term interest rates are not falling, which are typically signs of a pending recession/deceleration in economic growth.

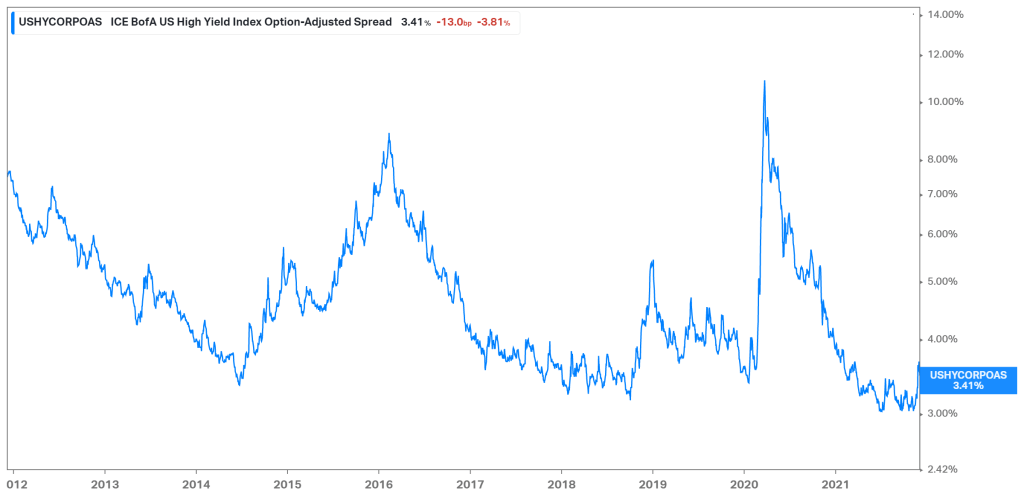

High yield credit spreads have widened from their recent lows but tightened last week and remain well below ranges typically associated with decelerations in economic activity and corporate profitability. The directionality and absolute level of credit remains an important indicator suggesting investors are not concerned about a slowdown in economic activity.

Source: Koyfin.

In the currency markets, the U.S. dollar index (DXY) declined last week but remains close to the highest level since mid-2020.

Source: Koyfin.

All developed market pairs have struggled against the U.S. dollar recently and the defensive currencies like the Yen and the Swiss Franc continue to be the best performers.

Source: Koyfin.

Within emerging markets, some oil-based areas (Mexico and Russia), South Africa (COVID variant and heavy commodity exposure), and some special situations like Turkey (not pictured) have lagged the U.S. dollar recently. Other countries like the Philippines, China, South Korea, Brazil, and India have been up or down less than 1% vs. the U.S. dollar.

Source: Koyfin.

In periods of time when investors expect economic growth to decline, emerging market currencies typically lag the U.S. dollar across all major pairs.

Within U.S. equity markets, the S&P 500 and the NASDAQ 100 are less than 5% below their all-time high levels reached at the beginning of November.

Source: Koyfin.

The Russell 2000 has been more significantly impacted and is down over 11% from the November high. This is likely due to the difference in liquidity and market beta of these securities.

Source: Koyfin.

Volatility levels for these indexes increased again last week and are near the highest level in the last twelve months. If volatility levels continue to remain at elevated levels, this could suggest the end of the recent rally and remain a key signal to monitor.

Source: Koyfin.

Energy and Financials have started to underperform which lines up with the decline in commodity prices and a flattening yield curve. This may be suggesting more of a rotation in leadership than an outright recession signal.

Source: Koyfin.

Last week, we mentioned that there will be some key markets to monitor to determine investor concerns about the new COVID variant. Several European countries have been experiencing rising cases and have implemented stringent policies. Polish and Austrian stock markets increased last week, stocks in the Netherlands continued to decline, and the German stock market ended the week flat (6.5% below the recent high).

Source: Koyfin.

Since the new variant originated in South Africa, we also thought it could be helpful to monitor movements in their equity market. South Africa was up 7% last week and was the best performing global equity market that we track.

Source: Koyfin.

Equity markets in China also increased last week and have been one of the best performing markets in the last month. They have very stringent COVID protocols and are very sensitive to changes in global economic activity. If their equity market starts to outperform, that could be another sign from investors that the new variant is not having an impact on economic growth.

Source: Koyfin.

It is still too early to tell what impact the new variant may have on economic activity. The market signals of the last few weeks are starting to suggest that investors think inflation levels are going to decelerate and yield curves are going to continue to flatten but that a recession is not imminent. This will negatively impact the performance of commodities and commodity linked securities as well as securities linked to steepening yield curves like financials/banks, but other industries could continue to experience positive performance.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC