The announcement of a new variant of COVID-19 contributed to a sizeable move across multiple asset classes last week. It is too early to tell what the impact will be on the economy going forward, so we will have to watch the market signals for guidance on what impact investors expect the variant to have on growth and inflation.

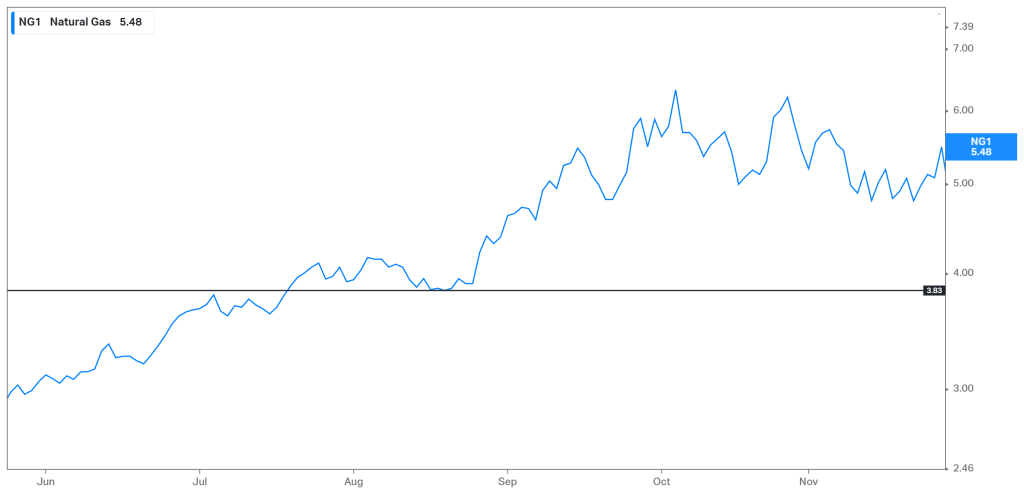

In the commodity space, energy-oriented areas like oil and natural gas have declined double digit percentages but are above their August lows (from the impact of the prior variant).

Source: Koyfin.

Oil volatility increased significantly along with the decline in price. We will have to continue to monitor this to determine if this is a temporary move (like the most recent examples) or something more significant.

Source: Yahoo Finance.

Agriculture based commodities like coffee, corn, and wheat increased last week, along with the overall agriculture index.

Source: Koyfin.

If investors become concerned about the outlook for economic growth and inflation, then all commodities should likely start to decline and experience lower highs and lows.

In fixed income markets, 10-year interest rates declined in the U.S. and across global developed market economies but remained above their August lows and within the same range as the last two months.

Source: Koyfin.

The ten-year/two-year yield curve in the U.S. got close to the recent low, while yield curves in other developed countries remain well above their August lows.

Source: Koyfin.

The MOVE index (which measures US Treasury volatility) continued to make new highs last week. Typically, Treasury volatility declines as investors start to price in a deceleration in economic activity and inflation.

Source: Merrill Lynch.

If investors begin to expect a significant slowdown in economic growth and inflation, long term interest rates will likely drop below the recent range and yields will likely make lower highs and lower lows, and the yield curve will likely flatten to new lows.

High yield credit spreads widened last week but remain well below ranges typically associated with decelerations in economic activity and corporate profitability. The directionality and absolute level of credit spreads will be an important indicator to monitor.

Source: FRED.

In the currency markets, the U.S. dollar index (DXY) has moved to the highest level since mid-2020 but was flat last week during the market volatility (declined slightly on Friday).

Source: Koyfin.

All developed market pairs have struggled against the U.S. dollar recently and the defensive currencies like the Yen and the Swiss Franc performed best last week.

Source: Koyfin.

Within emerging markets, some oil-based areas (Mexico and Russia), South Africa (COVID variant and heavy commodity exposure), and some special situations like Turkey (not pictured) have lagged the U.S. dollar recently. Other countries like the Philippines, China, and India have been flat vs. the U.S. dollar.

Source: Koyfin.

In periods of time when investors expect economic growth and inflation to decline, emerging market currencies typically lag the U.S. dollar across all major pairs.

Within the equity markets, major indexes within the U.S. are within a 2-8% of their all-time highs reached within the last two weeks.

Source: Koyfin.

Volatility levels for these indexes increased to end the week, and like oil volatility and high yield OAS, this will be something we have to monitor to determine if this will be temporary or the start of a new trend.

Source: Koyfin.

Source: Yahoo Financc.

Some key markets in Europe experienced rising cases and may implement mobility restrictions. This will be important to monitor going forward.

The German stock market made a new high mid-November and is 6% below that level.

Source: Koyfin.

The Austrian stock market made a new high in early November and is 9% below that level.

Source: Koyfin.

The Netherlands stock market made a new high in mid-November and is 5.5% below that level.

Source: Koyfin.

If the new variant is expected to impact economic activity on a sustained basis, these markets are likely going to lag.

Since the new variant originated in South Africa, it could be helpful to monitor movements in their equity market. That market was already declining prior to the variant news as local commodities had been declining, but a rebound in this market could be a positive sign in terms of the perceived impact of the new variant.

Source: Koyfin.

At this point, there is not enough evidence to determine what impact the new variant may have on economic growth and inflation and how that will be priced into financial markets. We will continue to update our cross asset class signals to determine if enough of them have started to move in a direction that provides a clear recommendation one way or the other.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC