The official confirmation that economic growth slowed in the third quarter was released this week as the GDP report showed that the annualized growth in Q3 was 2.0% compared to 6.7% in Q2. The year-over-year growth rate declined to 4.9% from 12.2%.

Source: FRED.

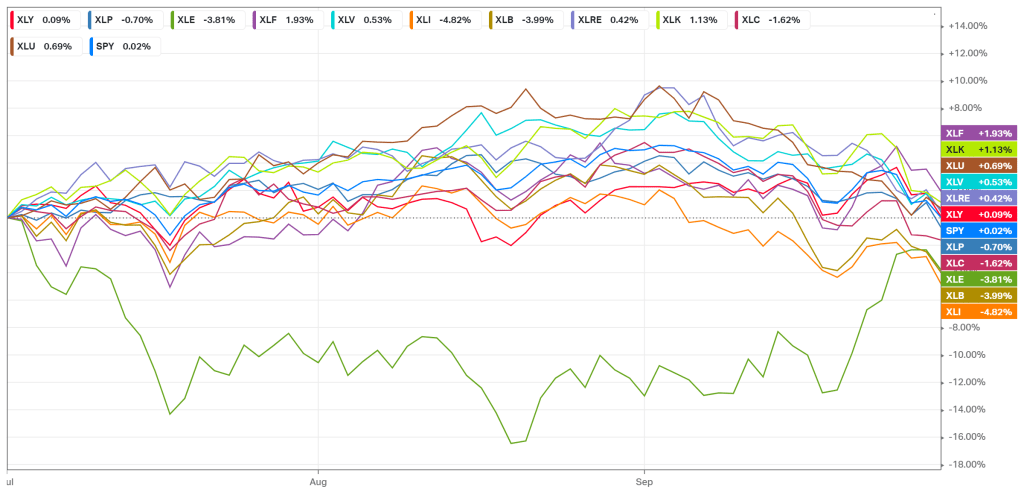

This decline in activity was well anticipated by investors and was one of the contributing factors to market performance in the third quarter (cyclicals, high beta, small caps equities lagged, interest rates declined, yield curves flattened, and the $US appreciated).

Source: Koyfin.

Economic data from the third quarter that has not yet been released will likely continue to confirm the slowdown noted in the GDP report. October economic data has started to improve and reflect an improving environment in the fourth quarter. The Conference Board’s Consumer Confidence Index rebounded 4.0 points in October to 113.8. This is the highest level in four months and both current conditions and expectations improved.

Source: Hedgeye.

Several of the regional manufacturing surveys were released last week and all of them reported month over month improvements in October (Dallas +10, Richmond +15, Kansas City +9, Chicago +5). This bodes well for the national survey which will be released on November 1st.

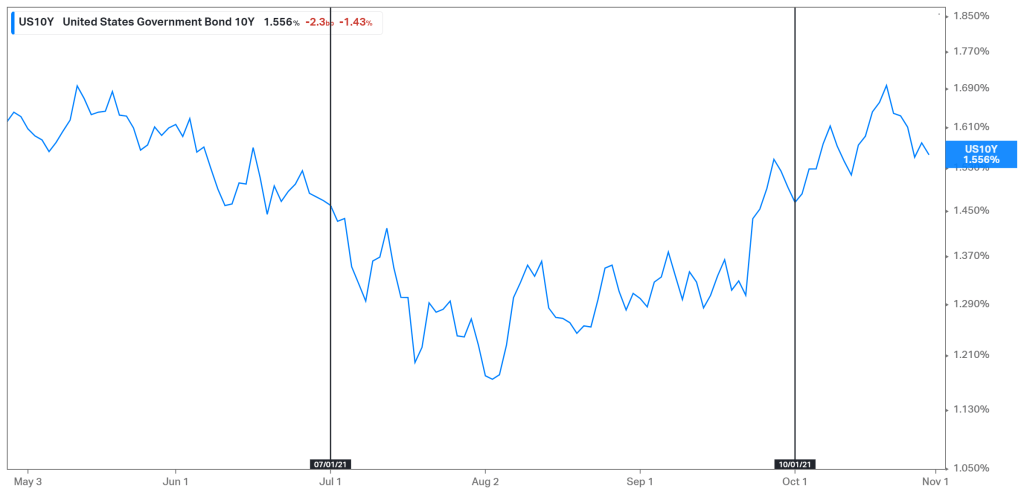

The market signals have been reflecting this improvement in fourth quarter data as cyclical industries are leading, momentum and high beta are outperforming defensive and low beta, ten-year rates and two-year rates have increased, and cyclical developed market currencies have been outperforming while the more defensive Japanese Yen has been underperforming.

Source: Koyfin.

Economic data will likely continue to improve in the fourth quarter, which market signals have started to reflect. Data from periods in the third quarter that will be released in the coming weeks are unlikely to impact market trends as these have already been discounted.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC