Economic data was light this week but continued to point to increasing economic growth and inflation. The Conference Board’s Leading Economic Index increased 1.3% and all ten components made positive contributions.

The Chicago Fed National Activity Index, which is comprised of 85 monthly indicators of national economic activity, increased to the highest level since July 2020. All four broad categories made positive contributions.

The April Markit Flash Manufacturing and Services PMIs were released, and both set series record highs, which continued strong growth from March. The Services PMI came in at 63.1, benefiting from a record increase in new orders, a strong increase in unfilled orders, and accelerating hiring activity. The Manufacturing PMI came in at 60.6, also benefiting from strong new orders, backlogs, and hiring.

Both reports noted a continued upward pressure on input prices but a higher ability to pass on the increase.

The consumer portion of the economy also continues to improve. The Langer Survey of Economic Expectations increased to a net positive optimistic view for the first time since February 2020. The weekly consumer sentiment index continues to make steady progress and currently stands at the highest level in over a year.

The labor market data showed mixed signs as initial claims continued to decline (a sign of a slowdown in layoffs), but total continuing claims increased back above 17 million (highlighting the delay in finding new work).

Source: FRED.

Source: Department of Labor.

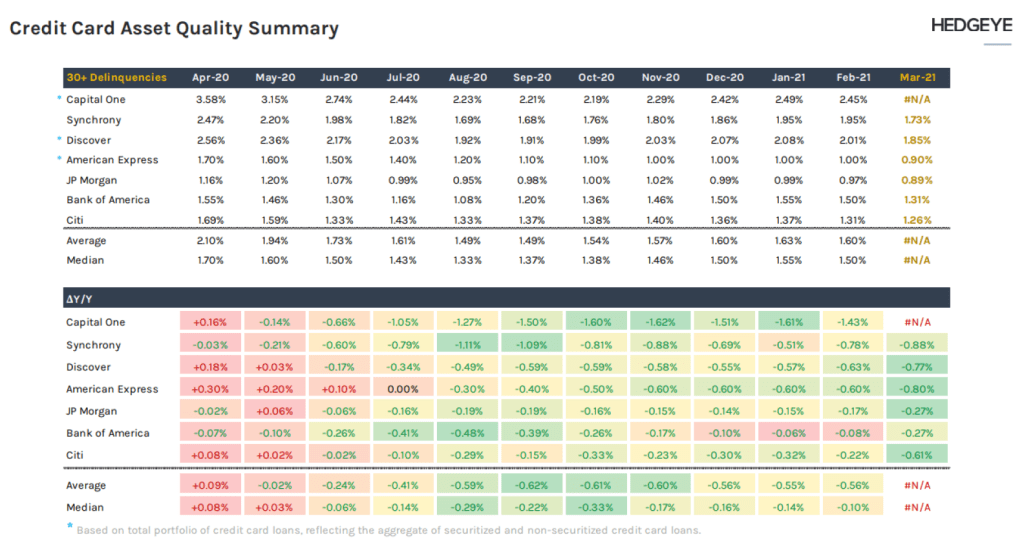

Credit card companies released their updated delinquency rate reports and the data showed continued improvement. This is a positive sign that the fiscal stimulus and slowly improving labor market are helping consumer balance sheets. This should be a positive for future consumer spending.

Source: Hedgeye.

From a market standpoint, the S&P 500 Index was positive for the week and closed just below a new all-time high.

Source: Koyfin.

The Russell 2000 small cap index was positive for the week and closed less than 4% from a new all-time high.

Source: Koyfin.

Equity volatility continued to decline with the VIX index (S&P 500) closing close to 17, VXN (NASDAQ) closing below 25, and RVX (Russell 2000) closing at 25.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

The U.S. dollar continued to decline, a trend that started at the beginning of the month and is near the middle of the range it has been trading in for the last six months.

Source: Koyfin.

The lower dollar helped the broad commodity index close at a new cycle high, moving above the top of the range it had been trading in since February.

Source: Koyfin.

High yield spreads widened during the week but are still very low and are not suggesting a change in investor risk appetite or concerns about corporate profitability.

Source: Koyfin.

Economic growth and inflation continue to move in the direction we expect to see for the next few months, which is leading to higher equity and commodity prices, as well as lower volatility.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC