Last week there was another increase in equity market volatility as the VIX Index traded above 30 intra-day on February 25th, up from 20 earlier in the month.

Source: Koyfin.

This same trend happened at the end of January. We reviewed other asset classes to see if the increase in equity markets was being confirmed broadly and could be a sign that investors were expecting economic and earnings growth to decelerate. Using that process, we noted that the volatility spike was unique to the equity market and not other asset classes. We are seeing a similar development today.

In the fixed income markets, High Yield bond spreads hardly moved during the week and are at the same levels as January 2020, before the impact of COVID in the U.S.

Source: Koyfin.

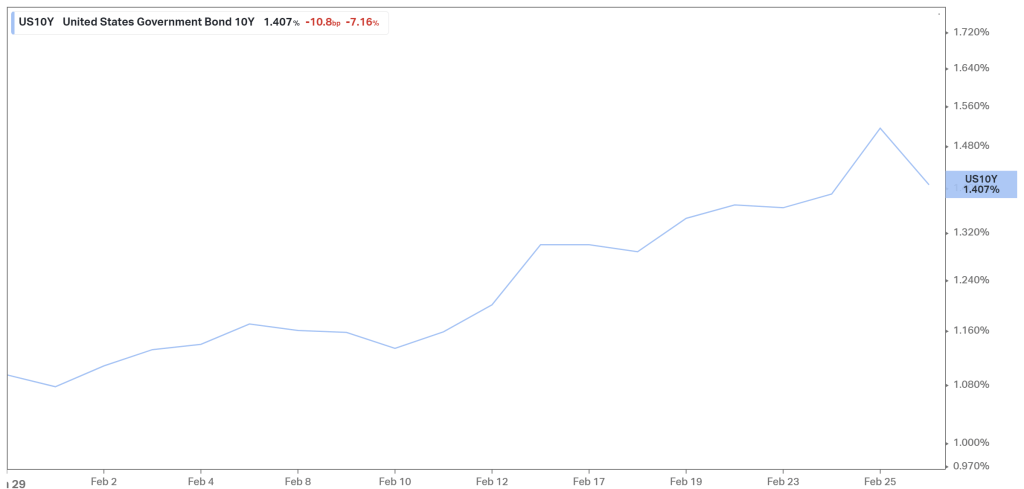

The interest rate on the 10-Year U.S. Treasury bond continued to increase last week. We have been writing about this trend for several months and view the increase in interest rates as a positive development, reflecting an improved outlook for economic activity.

Source: Koyfin.

Commodity markets continued to increase last week, as the broad commodity index closed near its highest level since October 2018. While oil volatility remained within the same range it has been since December, oil prices (WTI) closed at the highest level since the start of 2020, copper prices closed at the highest level since 2011, and the London Metal Index also closed at the highest level since 2011.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

In the currency market, the U.S. Dollar (DXY) moved higher during the week but is still lower than where it was at the beginning of February and is currently down over 11% from the recent high in March 2020.

Source: Koyfin.

Again, this data suggests that the recent increase in equity volatility is likely not an indication of a change in the outlook for economic activity.

There have been some recent developments in the equity market that warrant highlighting. While the VIX index moved from the 20s up to 30, volatility for the NASDAQ 100 Index (VXN) and some large components of that index like Apple (VXAPL) and Amazon (VXAZN) increased to 35-45.

Source: Koyfin.

From a performance standpoint, these mega-cap companies, and others like Tesla, have been underperforming recently.

Source: Koyfin.

At the same time, areas that have recently performed well are industries that were negatively impacted by COVID, including airlines, casinos, department stores/Retail REITs, hotels, restaurants, and oil companies.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

These industries are also heavily represented in the high beta factor ETFs, which are outperforming momentum ETFs. The momentum ETFs are heavily exposed to the mega-caps companies that we noted earlier.

Source: Koyfin.

The industries in these high beta indices should likely benefit from improving fundamentals as 2021 earnings are compared to 2020 and the economy opens back up. At the same time, the companies in the momentum index face tough comparisons in 2021 and are likely going to experience a slowdown in activity as consumer activity shifts to services and in-person activity. However, strong performance from these high beta industries versus momentum should be viewed as a positive, as these are highly cyclical/discretionary areas that tend to perform best when economic activity is accelerating. Volatility may increase and broad equity indices may decline as these mega-cap companies make up a large portion of the overall market cap, but this rotation toward areas that benefit from a decline in COVID restrictions is a healthy indicator for the economy.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC