Our macro research process involves making projections on the expected rate of change in economic growth and inflation over a one/two quarter period, then measuring and mapping economic releases and market signals to determine if we should be changing our view. The basis for this process is the historical relationship between asset class returns and volatilities during economic environments, categorized by the rate of change in economic growth and inflation.

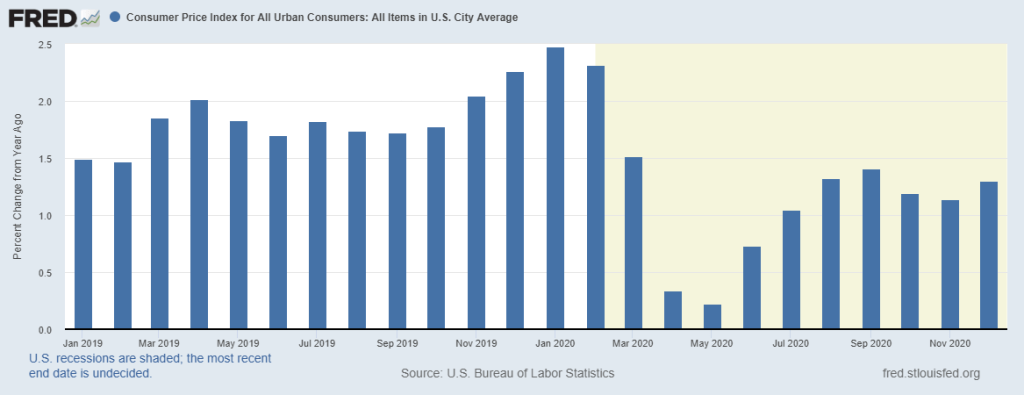

Since the end of November, we have been reiterating our view that economic growth and inflation would likely increase on a rate of change basis through the first half of 2021, and that many of the market signals were confirming this view. Much of the support for the view that growth and inflation will accelerate is the fact that they declined significantly in the first half of 2020.

Source: FRED.

Source: FRED.

There is a similar set-up for corporate earnings, as earnings growth expectations are rather strong due to the weakness in 2020.

This should likely continue to provide a supportive environment for cyclical/economically sensitive assets and a headwind for defensive and interest rate sensitive assets.

An additional part of our process is looking at the long-term trends in economic growth and inflation as well as the components of the economy that influence growth and inflation. When evaluating this data, it becomes apparent that growth potential in the U.S. and other major economies has declined on a structural basis since 2008. This trend is unlikely to change unless the policies put forth lead to an acceleration in private market activity.

The charts below show projected growth (blue line) over time using the average growth rate from the start of the data set until the end of 2007, compared to the actual growth (red line).

Source: FRED.

Source: FRED.

Source: FRED.

Source: FRED.

If growth and inflation continue at their lower trend level, this will likely lead to interest rates being lower than prior periods. While we expect growth and inflation to accelerate in the first half of 2021, which could lead to higher interest rates and a steeper yield curve, it will likely be at a lower level than prior periods.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

Source: Koyfin.

While we continue to expect the economy to improve in the first half of 2021, leading to improved corporate earnings and consumer incomes, and acting as a tailwind for cyclical versus defensive assets, we recognize that the longer-term economic trends are still negative. This should keep overall levels of growth, inflation, and interest rates below prior trends.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC