The S&P 500, oil, and credit markets have all rallied significantly over the last two months as states have lifted restrictions and economic data has stopped declining. There has been much discussion about whether this rally is sustainable and if it is the start of a new bull market. By looking at some short and intermediate term indicators, we will have a better idea of what they are signaling.

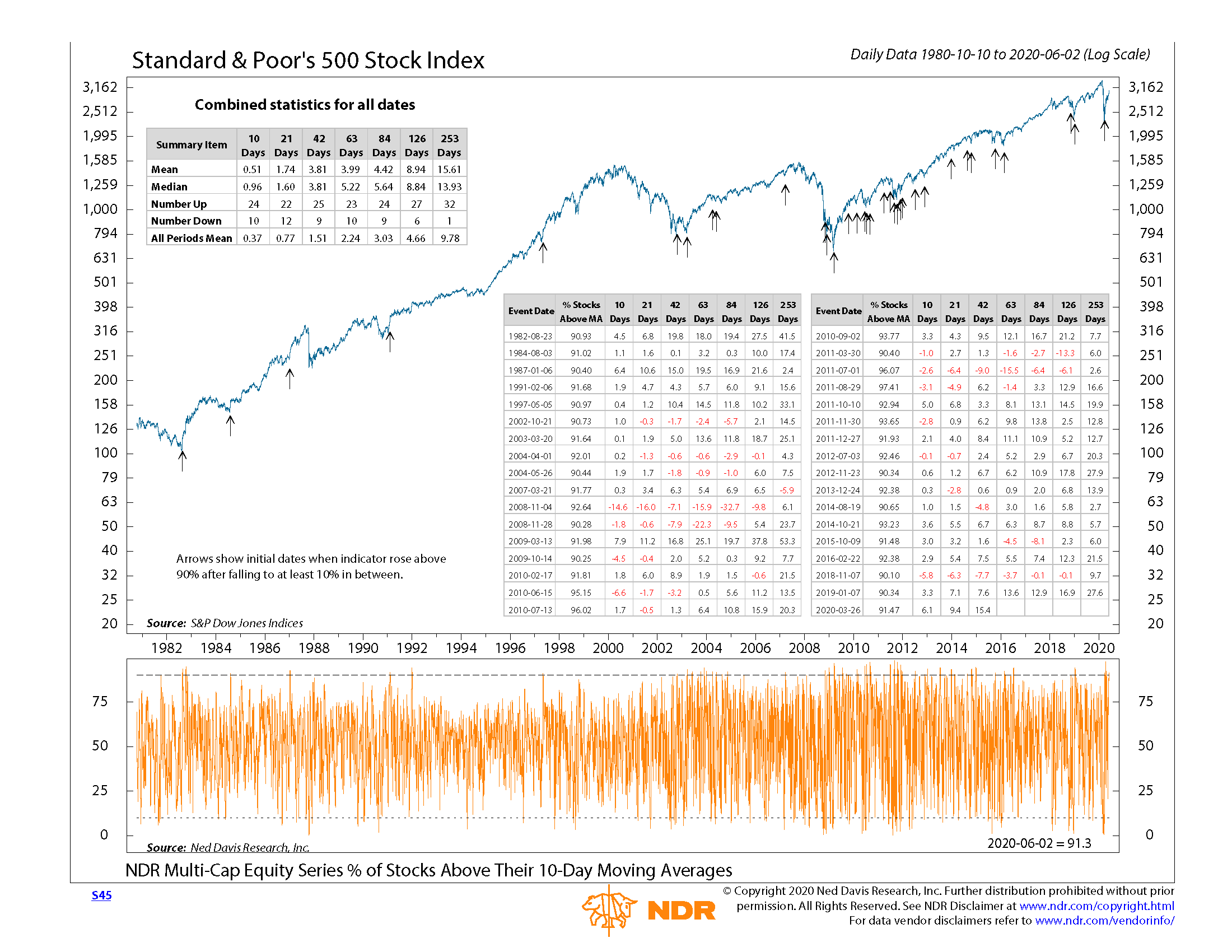

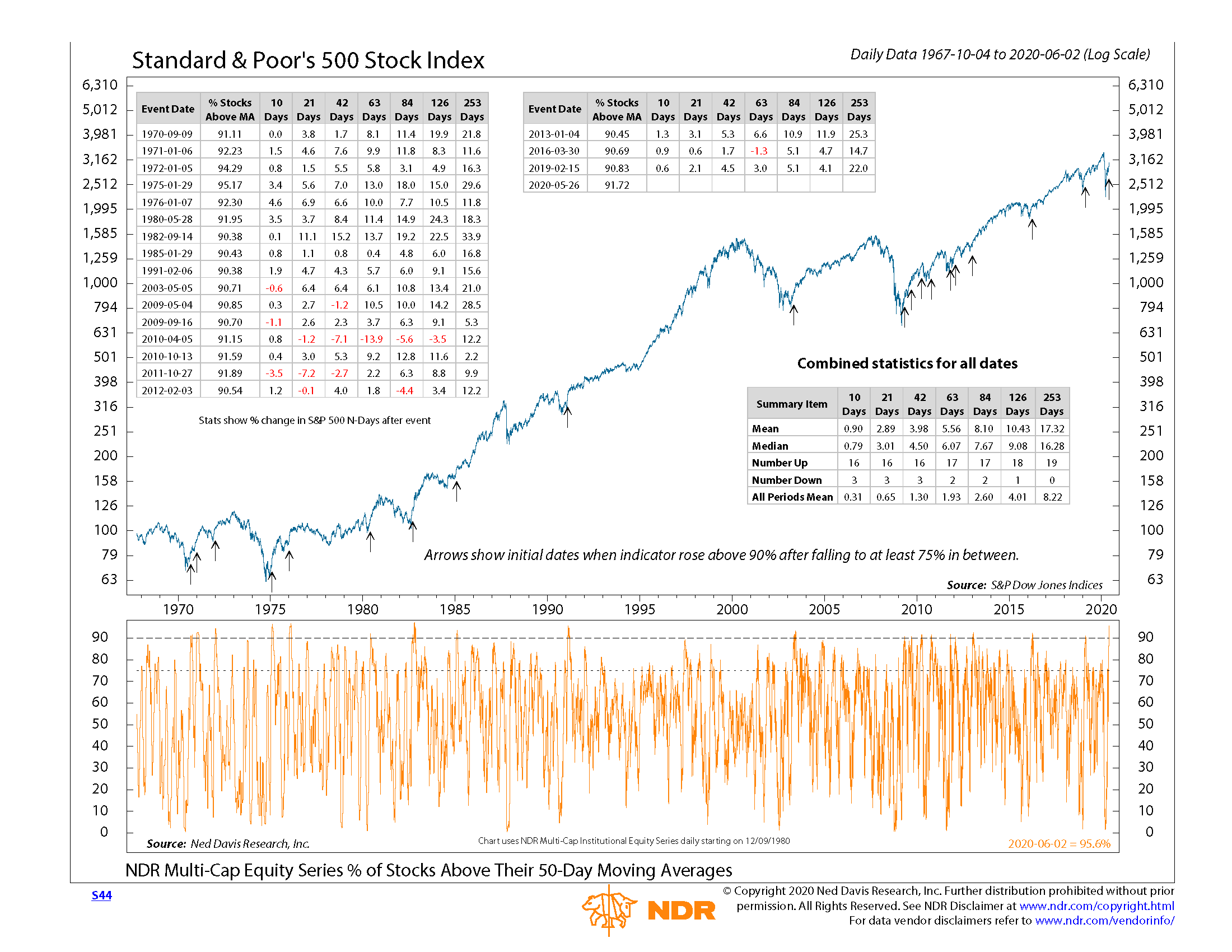

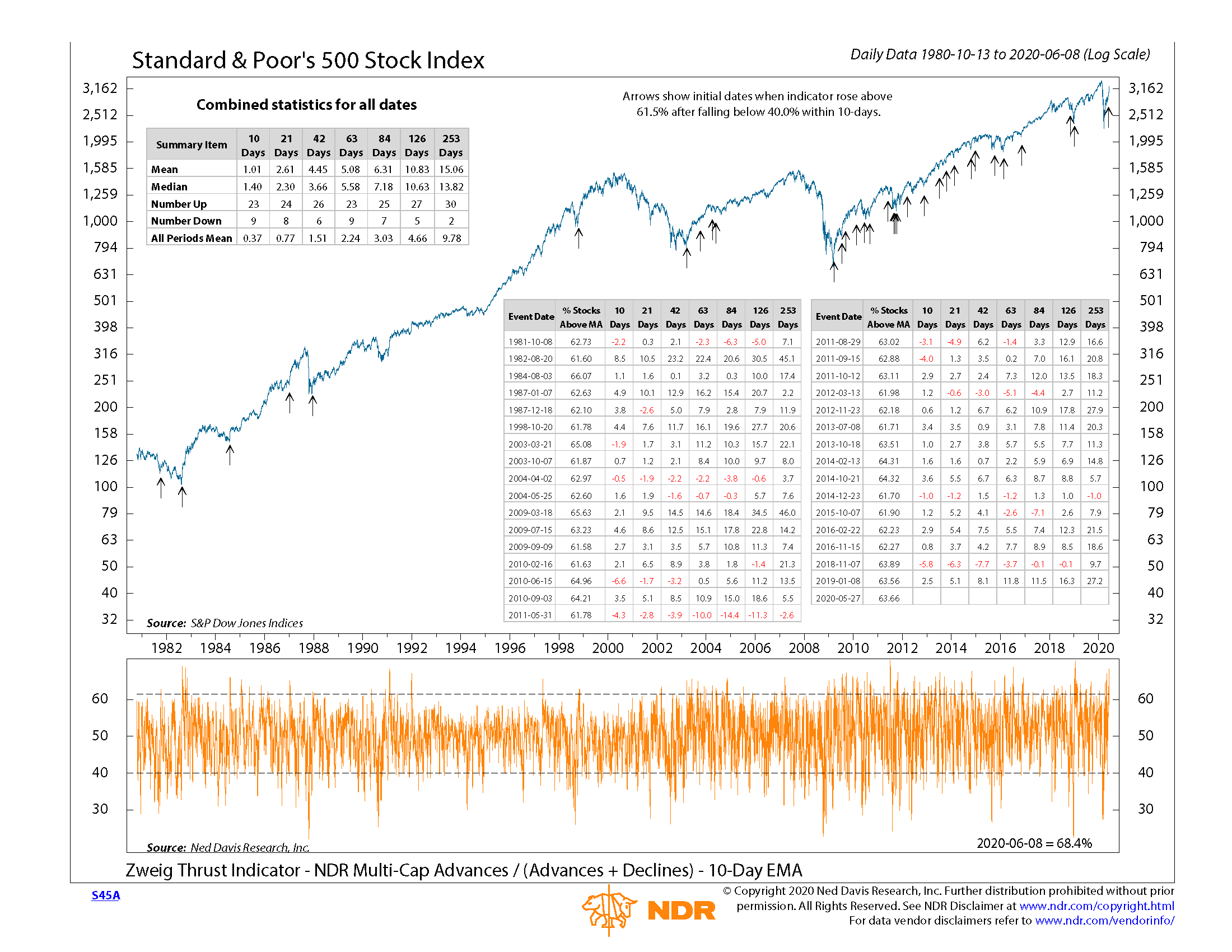

Short-term indicators are usually focused on momentum, sentiment, and breadth and are short term in nature, 10-50 days on average. These serve as good early signs that a large selling event has ended and that a new rally has started. As more of these signals turn positive, it has historically meant that the rally is gaining momentum and broadening, meaning that more stocks, industries, or countries are participating. As more segments of the market move towards positive trends, it increases the odds that the rally will continue because the positive momentum is not dependent on a small subset of participants. Looking at some of the short-term indicators that research firm, Ned Davis, tracks, we can see that most turned positive some time between March and May.

These positive signals likely mean that the low has already occurred (barring another lockdown or non-market-based event).

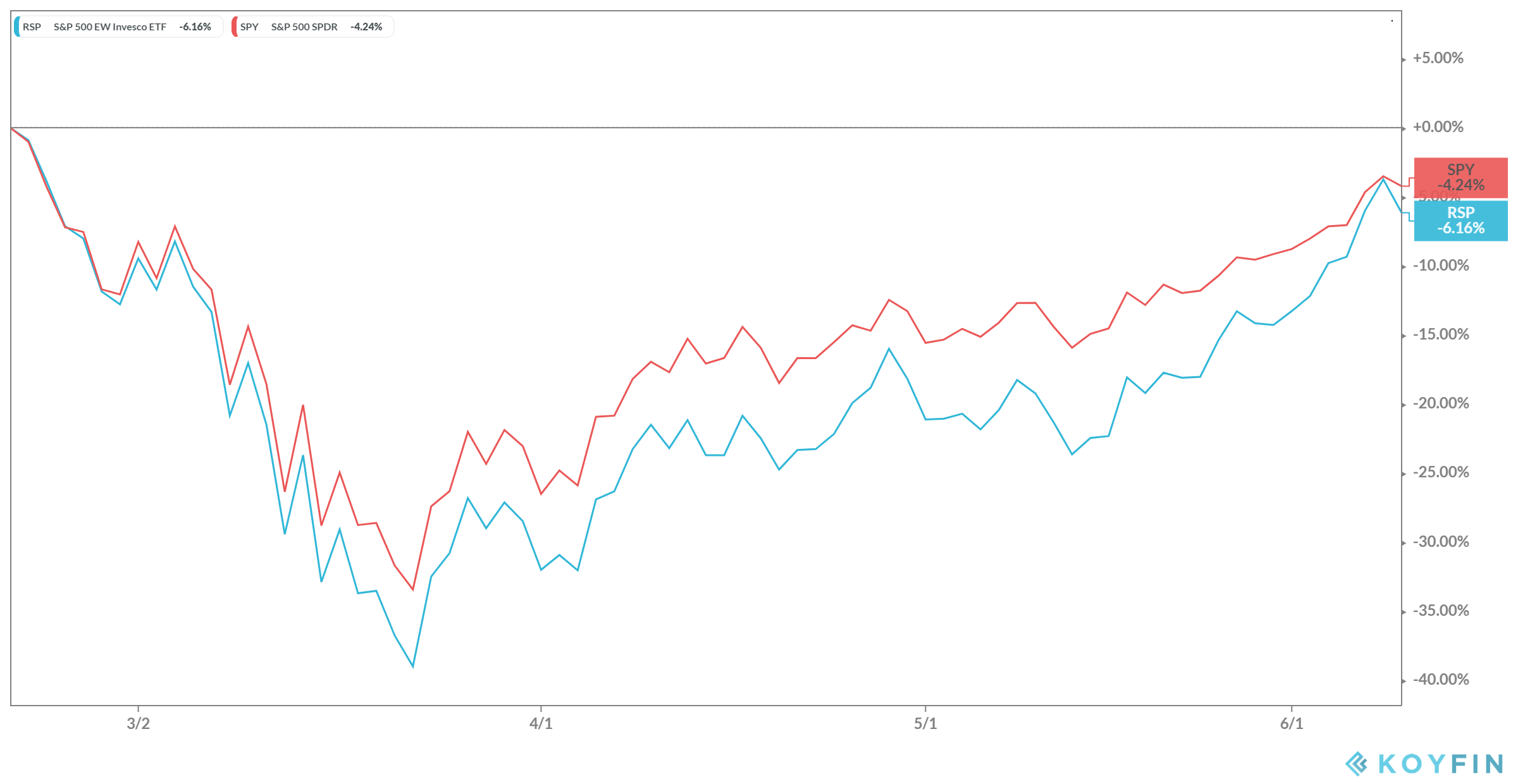

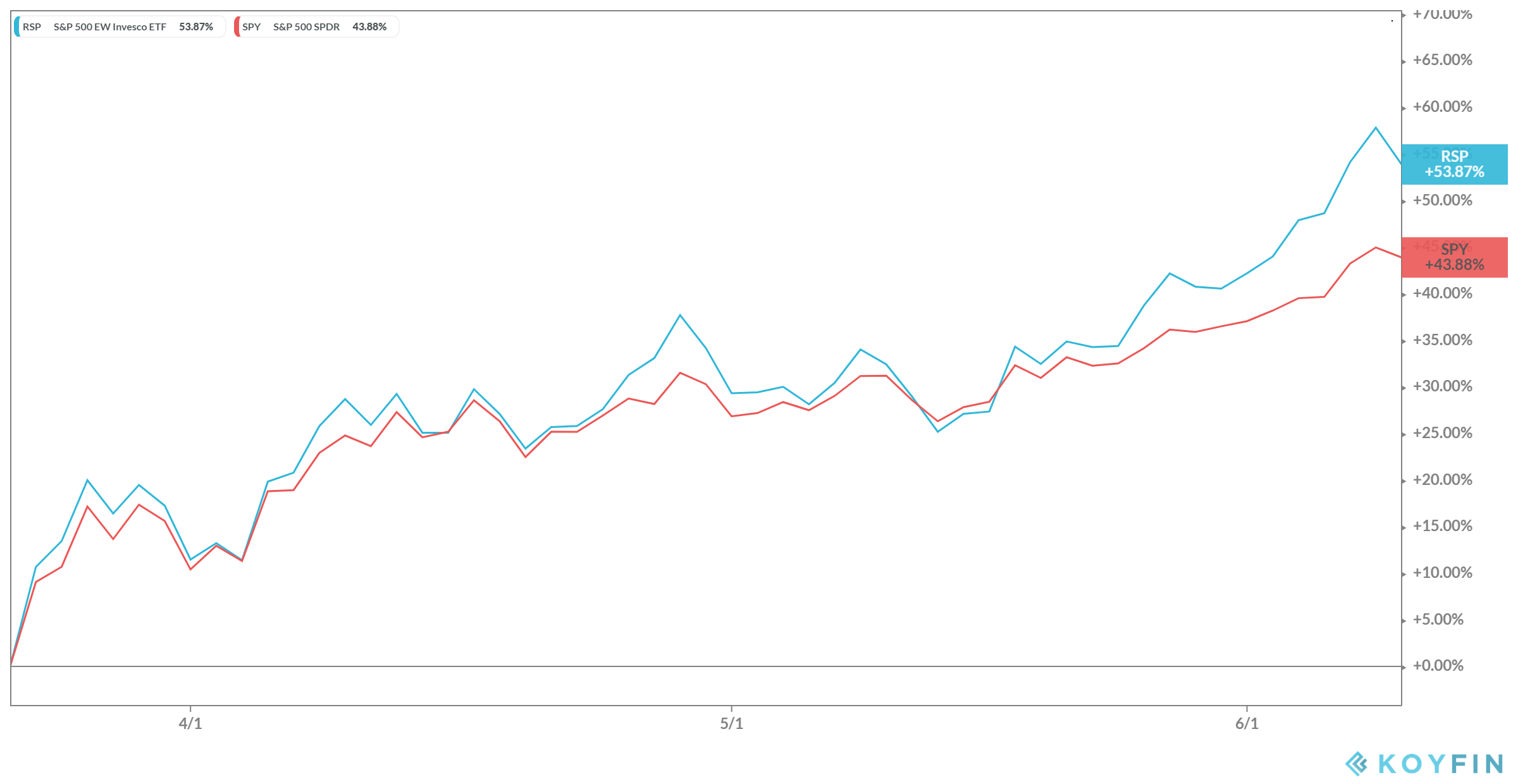

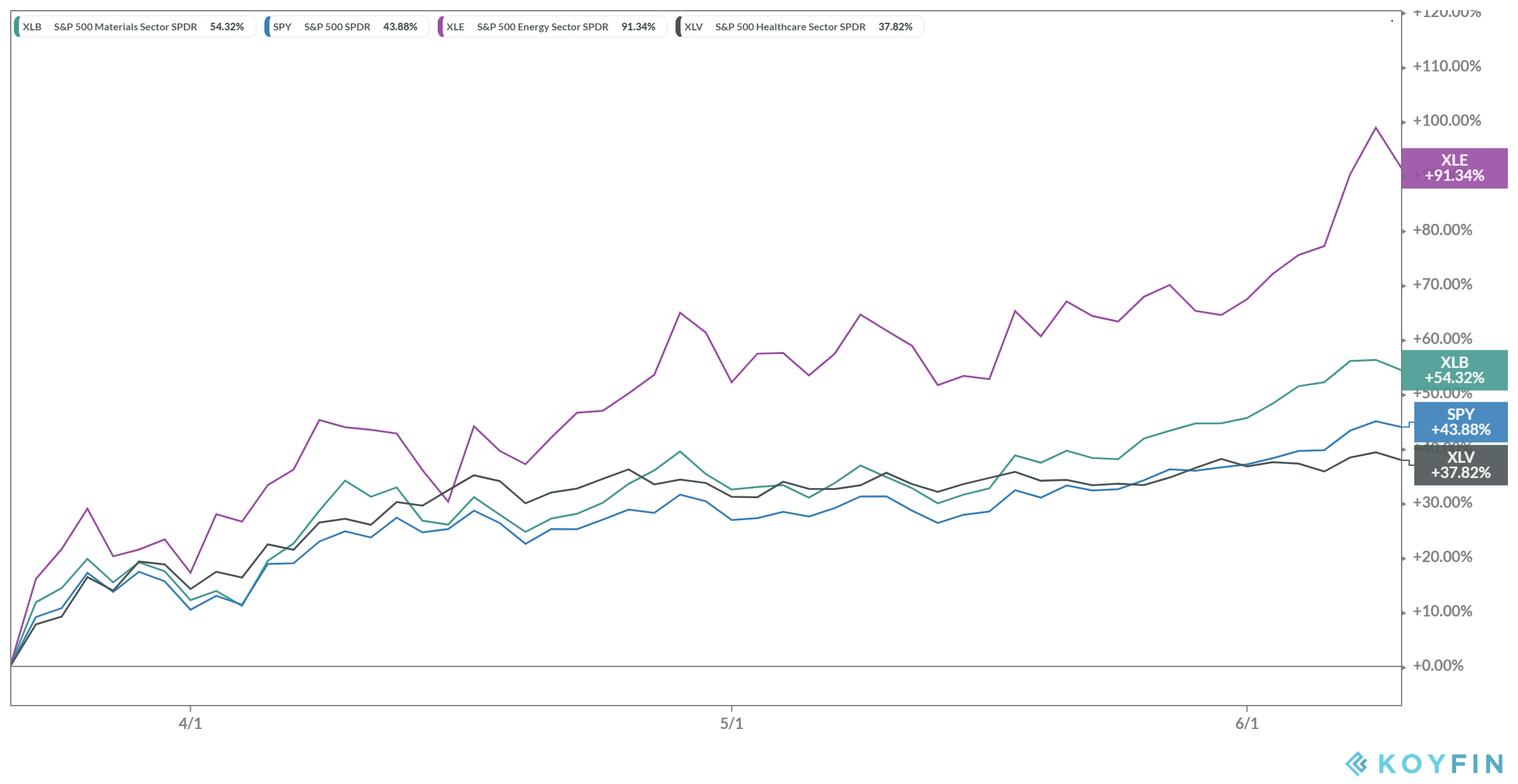

Looking at the returns of the market cap-weighted S&P 500 performance compared to the equal-weighted can also help identify if multiple sectors and stocks are participating in the rally. Returns since the February peak are not that dissimilar, and the equal-weighted index is outperforming since the March bottom. That is mostly a function of industries like Energy and Materials outperforming by a significant amount and being a much larger portion of the equal weight than the cap-weighted index and Health Care, which has lagged, being a smaller portion.

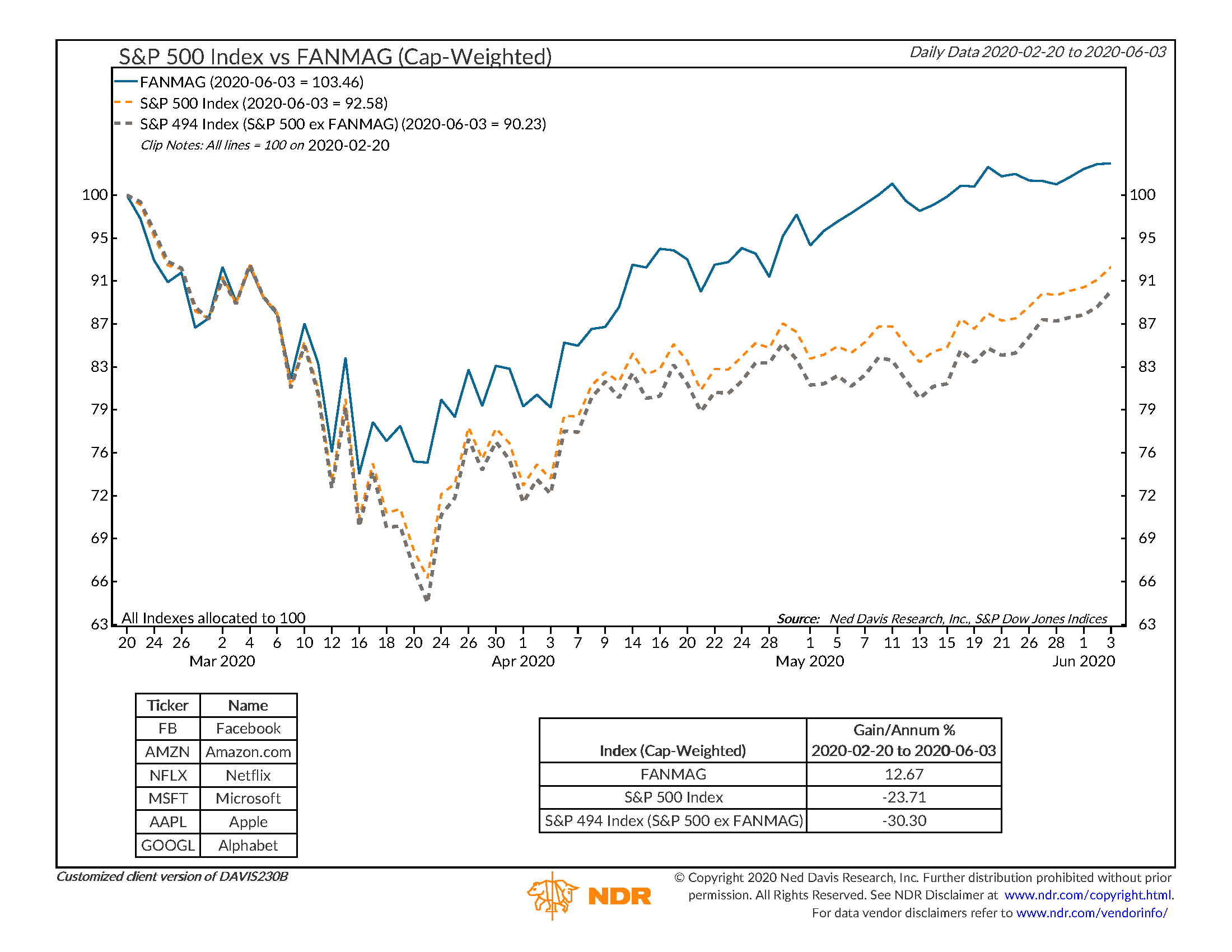

The performance at the stock level helps explain some of the strong performance of late. Comparing some of the largest stocks in the S&P 500 index (Facebook, Apple, Netflix, Microsoft, Amazon, and Google) to the remaining 494 stocks shows how much of an influence these mega cap companies have on the performance of the overall index. This is partly a function of how a market-weighted index works; the more the price increases, the larger the overall percentage of the total that stock represents. It serves as an indication that not all of the stocks in the index have recovered and likely states how much some of these businesses have been performing compared to the top six.

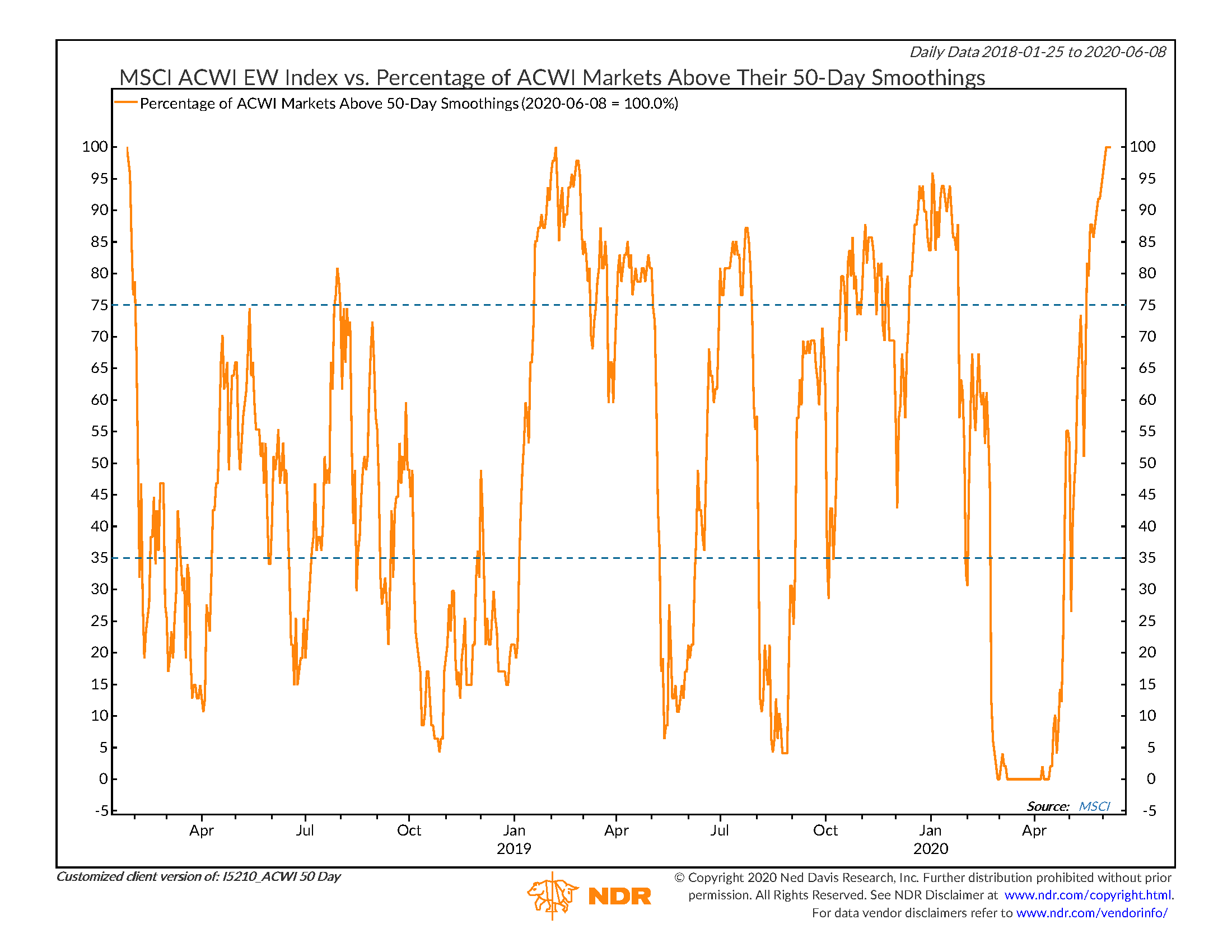

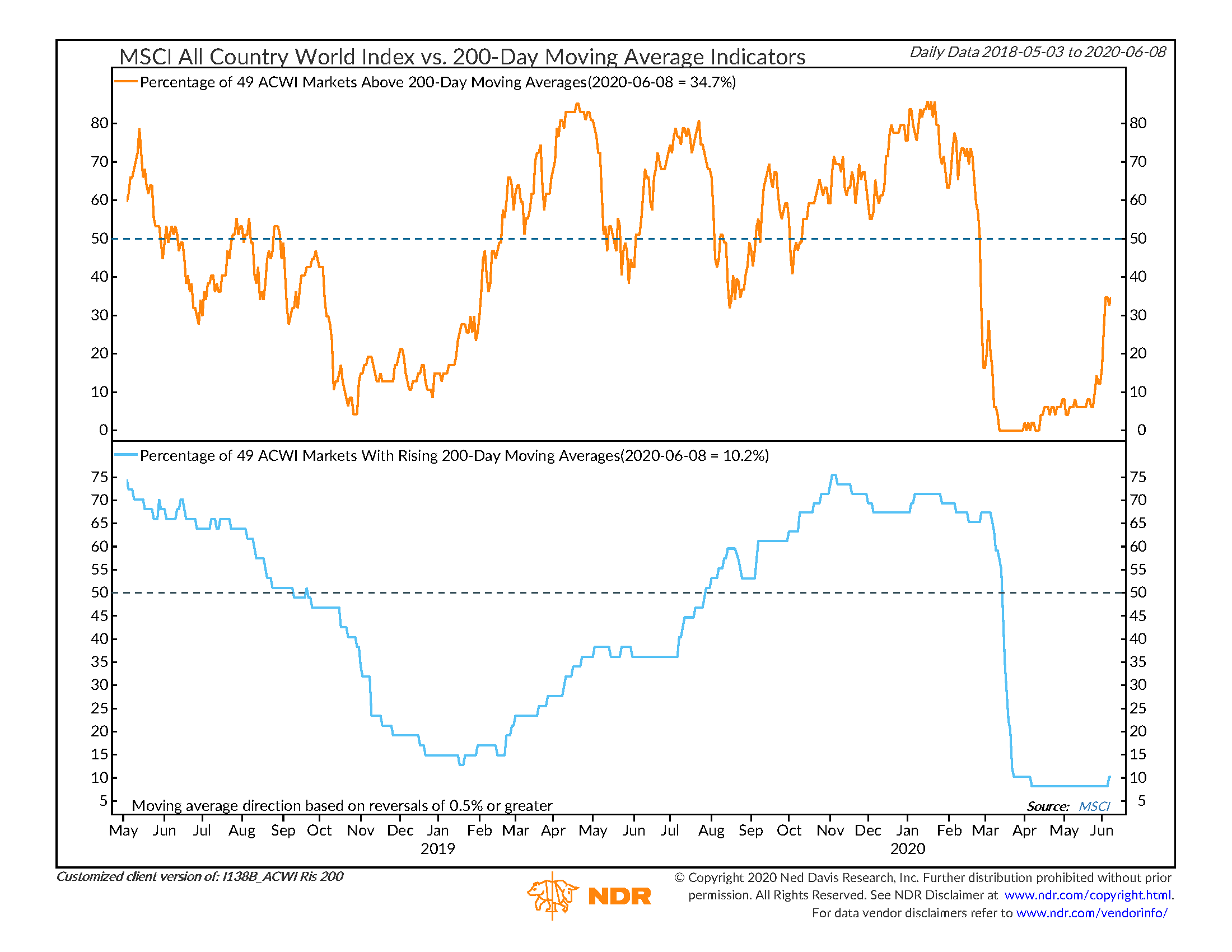

Intermediate and longer-term trends, typically 200 days to a year, help determine if the rally has been persistent enough for a sustained rally to take hold. This can be determined by looking at the percentage of stocks and regions above their 200-day moving average or with 50-day moving averages that are above their 200-day. The number of industries that have more than 50% of their underlying stocks above their 200-day also helps identify how broad the participation is in the rally. Many of these indicators have yet to reach levels that would suggest that the rally has reached a sustainable path that would warrant being fully allocated to higher risk assets.

There are some other indicators outside of price that can help determine whether the recent increase in momentum is sustainable. One is the economic data, which outside of mortgage applications, has improved but is still weak. If production and consumption can continue to increase and the economy starts to look like it can avoid any permanent damage, that should feed into corporate fundamentals and support higher risk asset performance.

Another set of indicators to monitor is asset class volatility. The volatility measure for the S&P 500 and Russell 2000 are still well above normal levels. Oil volatility is also very elevated. It is not uncommon for asset prices to experience wide swings when volatility is high. Typically, extended rallies in risk assets happen in periods of low and stable volatility. Volatility measures are coming down from their prior highs, and if this trend continues it could be another signal that the rally in risk assets can be sustained.

The views expressed herein are presented for informational purposes only and are not intended as a recommendation to invest in any particular asset class or security or as a promise of future performance. The information, opinions, and views contained herein are current only as of the date hereof and are subject to change at any time without prior notice.

Senior Vice President, Investment Strategy

Boyd Watterson Asset Management, LLC